09/26/2009

Professionals are moving towards substantial fair communication. Politicians are not yet.

I cannot be suspected of being complacent with professionals in Luxembourg.

I would like to underline a substantial change to their communication that deserves being congratulated.

In an interview last week, Jean Jacques Rommes said: "Je crois qu'il y a évidemment une sécurité, une confiance en nous-mêmes qui ont été ébranlées. Nous nous étions habitués, non seulement sur la place financière, mais dans l'économie luxembourgeoise en général, à des chiffres de croissance impressionnants, à des certitudes qui s'avèrent intenables à plus long terme. Je dois dire que, pour le principe, cela n'a pas tellement étonné l'ABBL. Sur le détail et sur la force de l'impact par contre oui. Nous avions toujours dit que les arbres n'allaient pas pousser jusqu'au ciel. Mais alors, que les racines les plus solides de la place financière se trouvent ébranlées comme cela, je vous avoue volontiers que je n'y aurais pas cru. Nous partageons à l'ABBL, le même ébranlement que doit ressentir l'homme de la rue, qui lui aussi s'était sans doute figuré que les choses seraient un peu plus solides que cela. Voilà pour l'impression. Ensuite, il y a les faits : Le fait que la place financière ne va plus générer à l'avenir les chiffres de croissance des dernières quinze années ; le fait que l'économie luxembourgeoise en général, ses budgets et les possibilités de l'État luxembourgeois devront s'adapter à cette donne ; le fait que la crise n'est pas terminée et que des impacts certains sur l'économie luxembourgeoise ne sont même pas encore ressentis" (free translation : I believe that there is obviously a safety, a confidence in ourselves which were shaken. We had been accustomed, not only in the financial center , but in the Luxembourg economy in general, with impressive figures of growth, certainty which prove to be intolerable longer-term. I must say that, for the principle, that did not astonish the ABBL so much. On the detail and the force of the impact on the other hand yes. We had always said that the trees were not going to push to the sky. But then, that the most solid roots of the financial center are shaken like that, I acknowledge you readily that I would not have believed it. We share with the ABBL, the same shock which the man in the street must feel, which him as had undoubtedly been appeared as the things would be a little more solid than that. Here is for the impression. Then, there are the facts: The fact that the financial center will not generate anymore in the future the figures of the growth of the last fifteen years; the fact that the Luxembourg economy in general, its budgets and the possibilities of the Luxembourg State will have to adapt to this situation; the fact that the crisis is not finished and that unquestionable impacts on the Luxembourg economy even are not felt yet) (Source: Land, 18 September 2009)

Jean-Jacques Rommes did a fair communication that demonstrate a risk awareness. Apparently, Luc Frieden goes on denying the seriousness of the crisis. He recently said: "Je note qu'actuellement la situation est en train de s'améliorer considérablement. Donc je crois que la place financière du Luxembourg n'a pas été fondamentalement affectée. » (free translation : I note that currently the situation is improving considerably. Thus I believe that the financial center of Luxembourg was not basically affected.) (Source: L’Echo, 22 september 2009)

Who is not telling the truth ?

Another professional did a fair communication that is more important in my opinion. It is about the Madoff affair.

Claude Kremer, Chairman ALFI, said: "Il y a un inventaire en cours de la façon dont chaque Etat applique la directive européenne sur les banques dépositaires. Ce n’est que lorsque cet inventaire sera terminé que l’on pourra voir où se situent les divergences. Nous sommes d’avis que le Luxembourg a transposé la directive comme il le fallait. Mais ces réflexions concluent à une harmonisation nécessitant quelques changements, nous serons évidemment demandeurs, à partir du moment où cela aboutit à abolir les différences entre les Etats." (free translation : There is currently an inventory of the way each State implements the European directive on depositary banks. It is only when this inventory is finished that one will be able to see where the divergences are. Our opinion is that Luxembourg transposed the directive as it was needed. But these thoughts conclude with a harmonization requiring some changes, we will be obviously in favour, as from the moment when that leads to abolish the differences between the States) (Source: Paperjam, 23 September 2009)

Claude Kremer is a smart lawyer. He perfectly knows the meaning of words. Before, the communication was that Luxembourg transposed the directive “failthfully”.

Claude Kremer said “as it was needed”, which is not the same meaning as “faithfully” and complies with the truth: the transposition was done as it was needed by the ALFI that has a very close and direct say on the evolution of the Luxembourg prudential regulatory environment governing the collective Investment Industry through a direct association with the Luxembourg Supervisory Authorities by means of a number of standing committees, where where it participates in the drawing-up and the interpretation of regulations.

As I explained in my Paper for the Consultation the word “faithful” was not acceptable as the synoptic table is clear enough to put substantial discrepancies on the spotlight.

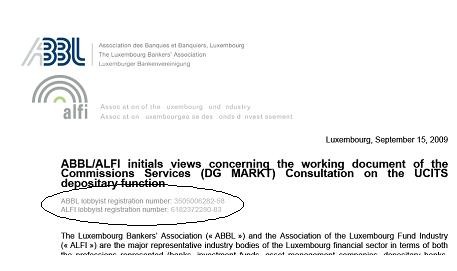

By the way, ALFI-ABBL has just published their initials views concerning the working document of the Commissions Services (DG MARKT) Consultation on the UCITS depositary function.

They present themselves as lobbyists.

It is amazing to observe that it seems it is the first time the ALFI uses the lobbyist number. I did not see this number on the other position papers (either responses to the CESR or to the European Commission).

In this document ABBL-ALFI do not address the key issues in Luxembourg.

They state that The Madoff affair is the wrong anchor for this discussion. It is premature to reach conclusions about any differences in the protection of investors among Member States until relevant court cases run their courses and the facts – and responsibilities for liability - are established.

I am afraid it is definitely the right anchor.

What do we have in Luxembourg?

Luxembourg Professionals present themselves as lobbyists whose opinion is practically an assent at least in Luxembourg.

I will quote again Rafik Fisher and the regulator.

“The Luxembourg Investment Fund Industry has regularly had a very close and direct say on the evolution of the Luxembourg prudential regulatory environment governing the collective Investment Industry (...) This influence has been exerted directly and indirectly by the lobbying initiatives taken on the level of the different professional associations, be it ALFI or ABBL , but also and more importantly, trough a direct association with the Luxembourg Supervisory Authorities by means of a number of standing committees" (Rafik Fischer, Vice Chairman, ALFI, in 2005, in an article called “Shaping the regulatory environment” that was publish in Fundlook, July 2005)

This is confirmed by the CSSF: "The internal committees assist the CSSF in the analysis of the development of the different financial sector segments, give their advice on any question relating to their activities and participate in the drawing-up and the interpretation of regulations relating to their specific field."

This is beyond an opinion, which would be normal. This is actually an assent.

Changes to the wording of the UCITS directive were decided

I suggest that the European Commission publish a synoptic table of the transposition in every jurisdiction to tighten up the ship and put is the spotlight what is practically the very close and direct say on the evolution of the Luxembourg prudential regulatory environment and the participation in the drawing-up and the interpretation of regulations.

Why some provisions were removed whereas others were added? Such changes are not observed in France or Ireland for example.

The consequence is drifts in Luxembourg

1. UBS acted both as Management Company and Depositary, which is explicitly prohibited by the directive, but not by the Luxembourg law..

2. The safekeeping duty was rephrased in a pragmatic way that is not compatible with the safekeeping duty as stated in the directive

Controls failed (regulator, auditor).

Read my analysis to the European Commission for details

I can conclude by quoting Einstein: We can't solve problems by using the same kind of thinking we used when we created them

17:58 Posted in Luxembourg | Permalink | Comments (0)

09/25/2009

The words that Claude Kremer, Chairman ALFI, did not say

Claude Kremer, Chairman ALFI, did a very interesting speech where he announced five initiatives.

He did not say anything about the Luxembourg Institute for GLOBAL Financial Integrity.

Two hypotheses:

- LIGFI is definitely dead despite someone is currently playing online with the website by testing layouts and launching a blog in a very professional way

- Professionals do not agree with LIGFI's stated objectives: it is amazing to observe that the LIGFI keywords fairness, responsibility and accountability are not quoted by Claude Kremer. Only transparency is quoted but one can respect transparency in a misleading way by not implementing the other keywords.

07:59 Posted in Luxembourg | Permalink | Comments (0)

OECD list

Monaco and Switzerland are no longer on the OECD "grey list".

But there is a huge difference : many agreements for Switzerland are with OECD members whereas Monaco signed with many fellow tax havens.

Since the last time the G20 met, in April in London, a few jurisdictions are said to move towards substantial implementation of tax information exchange.

Nothing is actually implemented.

30 countries have come together to build a task force to check the commitments. The head of the group is France's chief offshore tax hunter Francois d'Aubert.

06:00 Posted in General | Permalink | Comments (0)