06/01/2009

Pragmatism of deposit-guarantee schemes in Luxembourg

Directive 2009/14/EC of the European Parliament and of the Council was transposed in le Luxembourg legislation.

Luxembourg clear and pragmatic transposition of European directives is visible once more. Lucien Thiel was rapporteur of the law. He is one of the founders of the LIGFI.

The minimum coverage is not clearly increased as it appears that there is no budget to do so.

Additionally the wording of the transposition of one of the clauses of the directive is interesting.

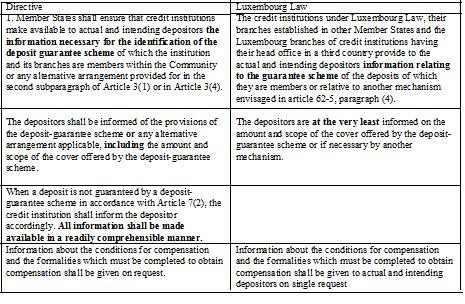

The directive states that “1. Member States shall ensure that credit institutions make available to actual and intending depositors the information necessary for the identification of the deposit guarantee scheme of which the institution and its branches are members within the Community or any alternative arrangement provided for in the second subparagraph of Article 3(1) or in Article 3(4). The depositors shall be informed of the provisions of the deposit-guarantee scheme or any alternative arrangement applicable, including the amount and scope of the cover offered by the deposit-guarantee scheme. When a deposit is not guaranteed by a deposit-guarantee scheme in accordance with Article 7(2), the credit institution shall inform the depositor accordingly. All information shall be made available in a readily comprehensible manner.

Information about the conditions for compensation and the formalities which must be completed to obtain compensation shall be given on request”

The Luxembourg law states that « (1) Les établissements de crédit de droit luxembourgeois, leurs succursales établies dans d’autres Etats membres et les succursales luxembourgeoises d’établissements de crédit ayant leur siège social dans un pays tiers fournissent aux déposants effectifs et potentiels des informations relatives au système de garantie des dépôts dont ils sont membres ou relatives à un autre mécanisme prévu à l’article 62-5, paragraphe (4). Les déposants sont pour le moins informés sur le montant et l’étendue de la couverture offerte par le système de garantie ou le cas échéant par un autre mécanisme. Des informations relatives aux conditions d’indemnisation et les formalités à remplir pour être indemnisés sont fournies aux déposants effectifs et potentiels sur simple demande »

Free translation : “The credit institutions under Luxembourg Law, their branches established in other Member States and the Luxembourg branches of credit institutions having their head office in a third country provide to the effective and potential depositors information relating to the guarantee scheme of the deposits of which they are members or relative to another mechanism envisaged in article 62-5, paragraph (4). The depositors are at the very least informed on the amount and scope of the cover offered by the deposit-guarantee scheme or if necessary by another mechanism. Information about the conditions for compensation and the formalities which must be completed to obtain compensation shall be given to actual and intending depositors on request”

Synoptic table :

The wording of the directive is changed, which opens the drift for a misleading communication:

- If the directive requires to provide “to actual and intending depositors the information necessary for the identification of the deposit guarantee scheme ”, the Luxembourg text states " to actual and intending depositors information relating to the guarantee scheme". The wording of the requirements is vague: "the information necessary" v. "information relating"

- If the directive requires that “depositors shall be informed of the provisions of the deposit-guarantee scheme or any alternative arrangement applicable, including the amount and scope of the cover offered by the deposit-guarantee scheme” the Luxembourg law only requires "at the very least" the amount and scope of the cover offered : the impact is not the same. Information that must be provided is larger in the directive.

- The provision of the directive “When a deposit is not guaranteed by a deposit-guarantee scheme in accordance with Article 7(2), the credit institution shall inform the depositor accordingly. All information shall be made available in a readily comprehensible manner” is not in the Luxembourg text.

These are facts of a misleading information that will be provided knowingly to the investor on deposit-guarantee schemes in Luxembourg: I am afraid the transposition does not comply with the principles of integrity, as stated by Jacques Santer for the launch of the LIGFI: transparency, fairness, responsibility and accountability in the financial sector.

This reminds me of the pragmatic transposition of the UCITS directive that opened the drift with Madoff, which is denied but definitely proven with a synoptic table.

18:51 Posted in Luxembourg | Permalink | Comments (1)

05/30/2009

Open letter to Cobus de Swardt, Managing Director, Transparency International, with an invitation to ask questions to Luc Frieden at the OECD Forum 2009

Dear Mr de Swardt,

I have seen that you will be speaker at the OECD Forum 2009 that will take place on 23 June 2009 especially in the framework of a workshop called “Promoting market integrity” at the sides of Luc Frieden, who is minister of Finance and Treasury of a tiny jurisdiction that claims not to be a banking, financial and judiciary haven and claims to be self regulated (see OECD or GRECO reports).

The objectives of “Promoting market integrity” were given in the Declaration of the Summit on Financial Markets and the World Economy that took place on 15 November 2008

Promoting Integrity in Financial Markets: We commit to protect the integrity of the world's financial markets by bolstering investor and consumer protection, avoiding conflicts of interest, preventing illegal market manipulation, fraudulent activities and abuse, and protecting against illicit finance risks arising from non-cooperative jurisdictions. We will also promote information sharing, including with respect to jurisdictions that have yet to commit to international standards with respect to bank secrecy and transparency.

Let’s analyse with a glance at public and official sources what Luxembourg’s situation is regarding these objectives all the more than the small size emphasizes issues and dysfunctions:

Bolstering investor and consumer protection

I am afraid the recent CSSF decision on UBS about Madoff and Luxalpha (28 May 2009) is not a good omen for investor and consumer protection.

In any other jurisdictions UBS would have been fined by the regulator. May be Stephen Timms, Financial Secretary, The Treasury, United Kingdom, who is speaker in your workshop will be able to explain how the FSA sanctions professionals to protect investors and clients (see fine tables in the UK on the FSA web site). But in Luxembourg it is not possible: the legal and regulatory framework is weak compared to what exists abroad (see what J.-N. Schaus admitted, who retired recently from the CSSF: The maximum of the fines is 12,500 euros. What is very weak taking the stakes into consideration; it is necessary to engage the reflection on increasing our power to sanction. It would be better indeed to have more means, especially taking into consideration what exists in other jurisdictions) and conflicts of interest are generalised. (In Paperjam, 20 March 2009)

Avoiding conflicts of interest

Because of the small size there are many conflicts of interests, many cases of "professional incest".

The direct consequence is the small number of crime cases or corruption cases, which are of concern in official reports (See Narcotic Control Strategy report and GRECO report Phase III about Luxembourg):

- “The scarce number of financial crime cases is of concern, particularly for a country that has such a large financial sector. The GOL should take action to delineate in legislation regulatory, financial intelligence, and prosecutorial activities among governmental entities in the fight against money laundering and terrorist financing.” (Cf. p. 342 of the Narcotic Control Strategy report 2009)

- “Certain lawyers stressed the importance of relationships and networks of persons in Luxembourg society, the difficulties faced by the police in dealing with complex economic and financial crime, particularly because of lack of legal and other resources, and the ease with which companies can be established in Luxembourg.” (Cf. page 18 of the GRECO PHASE III Report "Criminalisation of corruption" [theme I] in Luxembourg).

Additionally it was shocking that Luxembourg provided the FATF with a generous grant that has nothing to do with the normal funding of the FATF, nor the OECD. Recently Angel Gurria admitted that a grant to the OECD from a member state would be of concern (See interview in Le temps dated 18 April 2009: “I can even ask a Member State to grant this sum. But how the world will interpret this grant?”)

Such grants definitely compromise the recipient' ability to address issues freely, thoroughly and objectively as the recipient (either FATF or OECD) has a decision making power in favour or discredit of the giver.

Preventing illegal market manipulation

I have no public or official sources about any possible illegal market manipulation from Luxembourg.

Preventing fraudulent activities and abuse

The Luxembourg Institute for Global Financial Integrity was launched a couple of weeks ago. Among the founders is a Luxembourg powerhouse that stated publicly opinions that do not comply with the will to prevent fraudulent activities and abuse. The former chairman of the Luxembourg Bankers' Association (ABBL) and who was until recently advisor to its board, explained in the framework of the transposition of the second directive that offences such as forgery, use of forgery, false balance sheet, use of false balance sheet or unauthorised use of corporate property are vague and ambiguous (See ABBL report 2003 page 22 for instance). Last year the same professional stated that “It is not our duty to control if the tax payer was honest” (Le Temps, 27 February 2008)

In Luxembourg, there is no balance sheet database and there are many bankruptcies including dubious bankruptcies involving the same actors.

In Luxembourg, anyone can be statutory auditor (Cf. law of 10 August 1915 on commercial companies as amended). There are statutory auditors that are neither members of the IRE (institute of registered auditors) nor the OEC (institute of chartered accountants), including auditors registered in exotic jurisdictions and that only exist in the Luxembourg Corporate Registration.

Protecting against illicit finance risks arising from non-cooperative jurisdictions

There are many “red flags” in the Corporate Registration of offshore scams including with non-cooperative jurisdictions. Exotic companies, i.e. companies that are registered in non-cooperative jurisdictions, may be shareholder and/or auditor of Luxembourg-registered companies.

As I wrote, to determine illicit finance risks arising from non-cooperative jurisdictions, a couple of "red flags" should be taken into account:

- Does the company appear recently in the Corporate Registration in Luxembourg?

- Is there a turnover of directors?

- Is there a turnover of auditors?

- Is any exotic company acting as the statutory auditor of the Luxembourg-based company?

- Is the company and or the auditor only quoted in the corporate registration with no visible economic reality (an office mentioned in the yellow pages of its jurisdiction, a website, employees, brochures, Ads...)

Many dubious situations are visible in the “Mémorial C” including a case under investigation to bypass the OECD convention: Eurolux Gestion, which is based in Luxembourg and would have been used to bypass the OECD Anti-Bribery Convention, meets these “red flags”.

Information sharing, including with respect to jurisdictions that have yet to commit to international standards with respect to bank secrecy and transparency.

In a speech before the Luxembourg Parliament on 13 March 2009, Luc Frieden announced that Luxembourg will conclude Double Taxation Agreements that conform to the OECD Model Tax Convention, which means that this was not the case before. Conventions are being signed.

But it remains that the request of information must be made on concrete, clear and precise evidence of tax evasion which excludes any “fishing expedition”. This is a problem in Luxembourg as leaders support tax evasion:

- Cf. what stated Lucien Thiel, former director of the Luxembourg Bankers’ Association: “It is not our duty to control if the taxpayer was honest” (L’Essentiel, 27 February 2008)

- Cf. what stated Jean-Jacques Rommes, current director of the Luxembourg Bankers’ Association, to comment a tax evasion case: “It is not the banker who started” (RTBF, 19 February 2009)

Nobody in Luxembourg repudiated their “business doctrine” to get the money, which definitely favours frauds.

The OECD tax framework is not sufficient to counter seriously tax evasion (Cf. Swiss professionals quoted by Le Temps on 26 May 2009: “It will be, in practice, very difficult for the foreign tax authorities which apply the OECD standards to provide this degree of details; If Switzerland goes in the same line as Luxembourg, the result will not be so problematic at all for Switzerland. Banking secrecy will be relatively preserved, and the client will keep his/her tax ethics under control”).

May I ask you to ask Luc Frieden a couple of critical questions publicly about Luxembourg’s goals to seriously promote Integrity in Financial Markets?

- Why is it so difficult to enforce the criminal liability for legal persons, despite an injunction by the OECD last year? Consensus to change the Luxembourg constitution however was reached within a day last year.

- Even though UBS procedures were changed, a breach with the legal and regulatory framework was made. Why wasn’t UBS fined all the more than fines in Luxembourg are not dissuasive?

- Why were Public Research Centres (Lippmann or Tudor) and/or the University of Luxembourg not involved in genesis of the LIGFI (Luxembourg Institute for Global Financial Integrity) project, which is promoted by a company specialised in economic intelligence and professionals that never ever demonstrated a commitment to business ethics?

- The registration of the domain ligfi.org took place in December 2008 by Luxembourg-based intelligence and international security experts but this cannot explain the amount of EUR 40 000 for the start-up funding. How were those EUR 40 000 spent on the LIGFI project between September 2008 and April 2009 prior to the official launch?

- Are you ready to enforce a legislation to introduce a criminal liability for bankers that help to commit tax evasion, a clear one with no pragmatic (read deceptive) wording like "knowingly" that was introduced in the AML legislation of 2004, which makes lawsuits a long shot in practice as admitted by the Luxembourg FIU?

Yours sincerely

Jérôme Turquey

Consultant is business ethics and reputational risk

http://ethiquedesplaces.blogspirit.com

17:06 Posted in Luxembourg | Permalink | Comments (0)

Blasted Secrecy jurisdictions (update)

Switzerland and Denmark have agreed at a technical level to the extension of administrative assistance in tax matters under Art. 26 of the OECD Model Convention. The tax authorities of both States initialed a revised double taxation agreement (DTA)

Le temps reported that at the same time ,Switzerland and Luxembourg initialed as well revised double taxation agreement with no transparency.

The secrecy was intended to mislead France and the European Union prior to sensitive tax negociations and does not comply with Luc Frieden's recent statement that Luxembourg is a transparent financial center.

15:49 Posted in General | Permalink | Comments (0)