07/08/2009

The UK and France have released a declaration on global governance and development

The United Kingdom and France intend to cooperate closely to confront the political, economic and security issues of the 21st century. Pursuit of the reform of the governance of international institutions is a necessity if they are to be made more capable of meeting the challenges raised by international security and responding to the global economic crisis and under-development.

As far as financial centers are concerned there are a couple of paragraphs (keywords in bold):

France and the United Kingdom will also address the task of implementing the decision of the G20 concerning uncooperative jurisdictions and remain vigilant in ensuring that the 42 countries on the OECD “grey list” meet their commitment to apply international standards for the exchange of tax-related information. It is essential that we maintain the momentum set by the London Summit. We are therefore clear that where jurisdictions have not reached the standard of information exchange agreement by March 2010, they should be subject to coordinated international counter-measures agreed in London. Both our countries also stress the importance of combating tax evasion and undertake to combine our efforts to reinforce the coherence and effectiveness of international action in this domain. We agree that the threshold of 12 tax information exchange agreements should be seen as a starting point in the move towards greater tax transparency. If progress stalls we will expect the threshold to rise above 12, bringing those who have not made further progress back into the “grey list”. We will work together through the G20 to ensure that proposals are developed by the time of the next G20 Summit to ensure that developing countries can benefit from the new cooperative tax environment, including through a new multilateral tax information exchange agreement. We also call on the OECD to look at country by country reporting and the benefits of this for tax transparency and reducing tax avoidance.

The United Kingdom and France welcome the work underway to consider how the Global Forum on transparency and exchange of tax information can fully involve developing countries as equal participants and reform its governance, including to establish an effective peer review process to ensure effective implementation of the international standards, ahead of the Pittsburgh Summit. Successful development of this type of arrangement in the area of tax havens could provide a model for other areas where the OECD has a particular contribution to make to responding to global challenges.

France and the United Kingdom acknowledge the work undergone by the Financial Action task force (FATF) to revise and reinvigorate the process aiming at identifying uncooperative jurisdictions and call the FATF to proceed swiftly with its new review process in order to publicly name the jurisdictions that pose risks to the integrity of our financial system and apply counter measures where necessary.

The fight against non-cooperative jurisdictions should also encompass prudential regulations. We call on the FSB to swiftly assess jurisdictions against international supervisory and prudential standards and report back by September on their progress in identifying uncooperative jurisdictions.

07:18 Posted in General | Permalink | Comments (0)

07/06/2009

Letter to Peter De Proft, Director General of EFAMA

Peter De Proft, Director General of EFAMA, comments on the EU Commission’s launch of a public consultation on the UCITS Depositary Function:

“EFAMA very much welcomes the Commission’s consultation because we think it is absolutely necessary that investors have faith in the UCITS regulatory framework, and as the leading representative of the asset management industry in Europe, we are very happy to be consulted and to express our views in order to keep investors’ confidence in the UCITS’ brand.

We think that it is important that we have the opportunity to express EFAMA’s views of how European policy towards UCITS depositaries should best evolve.”

I sent the following e-mail :

Dear Mr de Proft

Further to the EFAMA press release dated 3 July where you state that “EFAMA very much welcomes the Commission’s consultation because we think it is absolutely necessary that investors have faith in the UCITS regulatory framework, and as the leading representative of the asset management industry in Europe, we are very happy to be consulted and to express our views in order to keep investors’ confidence in the UCITS’ brand. We think that it is important that we have the opportunity to express EFAMA’s views of how European policy towards UCITS depositaries should best evolve.”, I would like, as a rigorous stakeholder, to stare my views with you.

I agree without any reserve to state that it is absolutely necessary that investors have faith in the UCITS regulatory framework and that it is critical to keep investors’ confidence in the UCITS’ brand.

But I am quite surprised by the way the ALFI and the EFAMA are handling the Madoff issue.

When discrepancies are clear enough, it is better to make amend and take initiative to build or rebuild trust than denying and/or hushing up the issue: a jurisdiction should not communicate on its fully compliant legal and regulatory framework and on the faithful transposition, when a basic analysis to compare the directive and the law and related regulations demonstrates that critical provisions explicitly stated in the UCITS directive were clearly dropped in transposition all the more than these missing provisions definitely opened the drift.

As I wrote, The base of funds is confidence, and the base of confidence is the truth.

Please find attached the current draft of my analysis of the Commission’s working paper on the UCITS depositary function, where I demonstrate to what extend an inaccurate transposition of the directive in Luxembourg opened the drift.

The expression "fully compliant" or "faithfull" to qualify the Luxembourg legal and regulatory framework vis-à-vis the UCITS directive are definitely not acceptable.

I am looking forward to hearing from you soon.

Best regards

Jérôme Turquey

Consultant in Business Ethics and Reputational Risk

http://ethiquedesplaces.blogspirit.com

18:51 Posted in General | Permalink | Comments (0)

07/05/2009

Organisational requirements: the Luxembourg fallacious transposition and communication

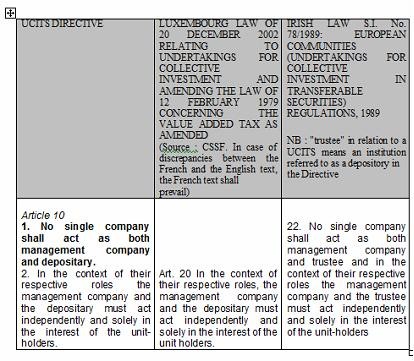

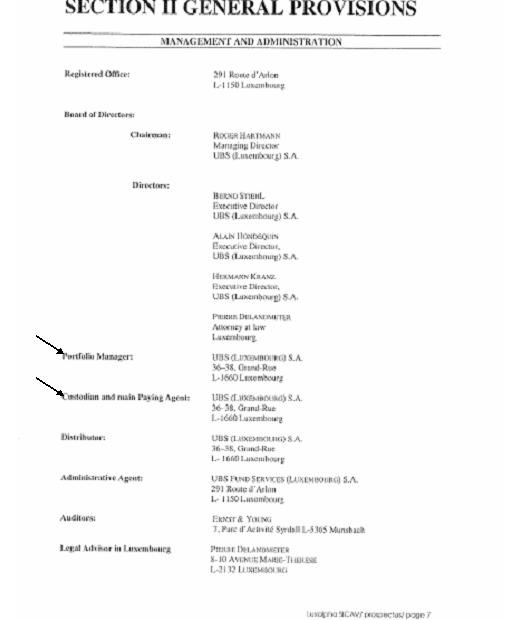

The working paper observes that “on the rules applicable to conflicts of interest, the amended UCITS Directive only sets principles of separation and ethical independence between the fund manager and the depositary in particular, Article 25 of the amended 85/611/EEC UCITS Directive - which reproduces the existing Article 10 of Directive 85/611/EEC – provides that: ‘no single company shall act as both Management Company and depositary (…) in the context of their respective roles the management company and the depositary shall act independently and solely in the interest of the unit-holders’. Depositaries may face situations where they can no longer ensure that they act solely and exclusively in the interest of unit-holders.”

The so-called clear and pragmatic rules in Luxembourg do not require that no single company shall act as both Management Company and depositary.

NB: In French documents Custodian is translated by Depositary.

The Requirement to prevent conflicts of interest, and especially the one of Management Company and Depositary that is explicitly stated in the UCITS Directive, was definitely dropped in Luxembourg despite a communication on the faithful transposition of the UCITS directive

19:58 Posted in General | Permalink | Comments (0)