04/11/2009

Bad news for Luxembourg

In an article a couple of months ago I reported that the Luxembourg jurisdiction was involved in a fraud through the subsidiaries of Icelandic banks in Luxembourg: hundred holding companies registered on the island of Tortola would have been established by Icelandic individuals through the subsidiaries.

As I said the Luxembourg tax haven is there.

Judge Eva Joly will be responsible for the investigation to tighten up the ship.

Two jurisdictions are involved: one the one hand Luxembourg that is on the OECD grey list, and on the other and the UK (London) that is on the OECD white list.

Know more:

Iceland review

Hundreds of Icelandic Companies Registered in Tortola

Iceland Hires International Corruption Hunter

Iceland’s Special Prosecutor Gets reinforcements

L’essentiel

Elle va traquer les capitaux islandais

09:53 Posted in Luxembourg | Permalink | Comments (0)

04/10/2009

CES report in Luxembourg: an insulated view of the crisis in the jurisdiction

The Conseil Economique et Social published its report.

The report is about the financial crisis and its level is much better than the parliamentary report on the financial crisis that was published a couple of weeks ago.

Nevertheless, the insulated culture remains and the authors never wonder why there is a problem in the Luxembourg jurisdiction.

The wording of a couple of paragraphs is worth commenting:

"Que ce soit le passeport européen des sociétés de gestion d’OPCVM, que ce soit l’architecture de la supervision européenne, que ce soit la fiscalité de l’épargne, il y a toujours des intérêts économiques et politiques manifestes derrière les attaques contre la réputation de la place financière luxembourgeoise."("Whether it is about the European passport for UCITS, whether it is about the architecture of the European supervision, whether it is about the savings tax, there are always obvious economic and political interests behind attacks against the reputation of the Luxemburg financial center")

It is a frequent argument in the language of many professionals in the Luxembourg: the jealousy of the other countries. They do not admit that there are dysfunctions in Luxembourg that create an unfair competition with other jurisdictions, especially in the European Union.

One cannot have the advantage of an “onshore jurisdiction” thanks to the membership in the EU, and of an “offshore jurisdiction” by offering the same services as a tax haven, and especially the possibility to create scams linked to exotic jurisdiction without any control.

This is what many fiduciaries located in Luxembourg sold and still sell.

"Les cercles intéressés français ont prétendu que la protection d’investisseurs à travers des fonds luxembourgeois serait plus faible qu’ailleurs en Europe, notamment à cause du niveau de responsabilité des banques dépositaires. Cette question a pu être partiellement désamorcée par les associations professionnelles et par les autorités luxembourgeoises, mais il reste que la réputation de la place financière a pour la première fois, été fortement ébranlée dans le domaine d’activités des fonds d’investissement."("The French interested circles claimed that investors' protection through Luxembourg investment funds would be weaker than anywhere else in Europe, in particular because of the level of responsibility of the depositary banks. This question could be partially defused by the professional associations and by the Luxemburg authorities, but it remains that the reputation of the financial center has for the first time, been strongly shaken in the field of activities of investment funds.")

The Luxembourg fund industry was not touched by chance by the Madoff case, but was made possible by the ‘Luxembourg-made” transposition" of the UCITS directive.

Facts are that:

- Two provisions of the directive that are connected to the Luxalpha case were not transposed into Luxembourg law : the one that states that unit trust's assets must be entrusted to a depositary “for safekeeping” (this explicit notion of “safekeeping” is not in the French version of the Directive) (Cf. French text page 15 v. English text page 15) and the one that states that “No single company shall act as both management company and depositary”.

- The depositary’s liability is limited by the wording of the supervision authority in circular IML 91/75 : "The concept of custody used to describe the general mission of the depositary should be understood not in the sense of “safekeeping”, but in the sense of “supervision” which implies that the depositary must have knowledge at any time of how the assets of the UCI have been invested and where and how these assets are available (…) As regards the extent of the duty of supervision of the depositary, one can consider that the depositary has discharged its duty of supervision when it is satisfied from the outset and during the whole of the duration of the contract that the third parties with which the assets of the UCI are on deposit are reputable and competent and have sufficient financial resources” : Madoff was definitely reputable and competent and had sufficient financial resources.

By denying their lax transposition, I am afraid that the Luxembourg professionals unfortunately weaken the funds industry in Europe and their own reputation: a fault confessed is half redressed.

“De façon plus générale, le Luxembourg devra maîtriser la vague réglementaire qui suivra la crise. Il n’est pas exclu qu’il puisse même prendre avantage dans le contexte actuel sur les centres offshore entièrement déréglementés. » ("In a more general way, the Luxembourg will have to monitor the regulatory wave that will follow the crisis. It is not excluded that it can even take advantage in the current context of the fully deregulated offshore centres.")

It is clear enough that the Luxembourg professionals are not willing to abide to regulation. The professional culture is that they want a pragmatic implementation, like for the UCITS directive.

Above all, by reading between the lines one understands that Luxembourg is an offshore center that is not totally deregulated, which means that it is partially deregulated. And it is true.

In a nutshell, the behaviour of the jurisdiction with Juncker’s crusade against the OECD and the USA while not questioning the dysfunctions in the jurisdiction, is a business suicide.

15:06 Posted in Luxembourg | Permalink | Comments (0)

04/05/2009

The mask fell: Luxembourg pressure on the OECD at the great day (update)

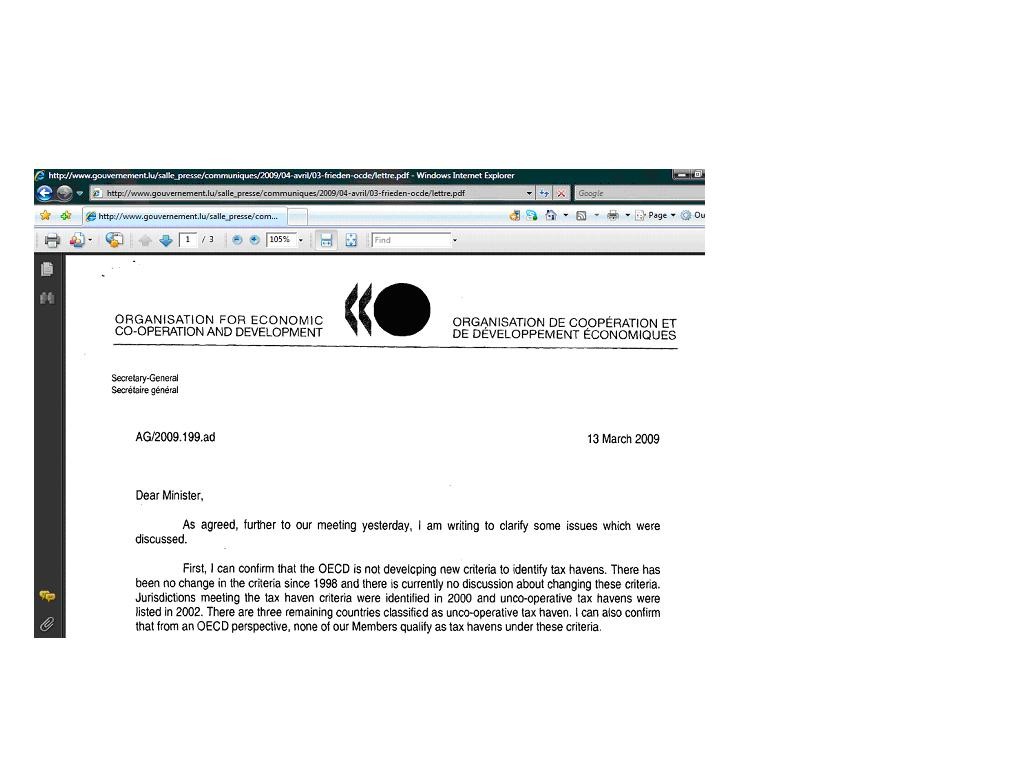

The Luxembourg government published a letter from Angel Gurria to Luc Frieden

By publishing this letter the Luxembourg government shows how politics influence the OECD policies:

Let’s read a couple of paragraphs:

I can confirm that the OECD is not developing new criteria to identify tax havens

I can also confirm that from an OECD perspective, none of our Members qualify as tax havens under these criteria

In formulating their requests, competent authorities should demonstrate the foreseeable relevance of the requested information. It would, for instance, not be possible for a State to request information randomly on bank accounts held by its residents in banks located in the other State.

This is definitely a political fault as it is an awkward operation that is intended to make pressure on the OECD to prevent any sanction against Luxembourg and any evolution to the OECD criteria.

It is not the first time that the Luxembourg government makes public a letter to make pressure. Last October, Arlette Chabot, information director for French TV station France 2, had written an apology to the Luxemourg Prime Minister, Jean-Claude Juncker, after her station suggested that not all is well in the jurisdiction. The letter was not intended to be public and Arlette Chabot was surprised. The communication was intended to discourage questions on Luxembourg

As far as the publication of Gurria's letter is concerned, it allows Luxembourg not abide by the commitments taken as none of the OECD Members qualified as tax havens when the letter was written all the more than the OECD is not developing new criteria to identify tax havens.

06:41 Posted in Luxembourg | Permalink | Comments (0)