02/12/2009

Madoff case and the crisis communication of the financial regulator: Luxembourg: 7 – Ireland: 1

In my past articles I have underlined that the CSSF, the Luxembourg regulator, and the financial center of Luxembourg in general had and stil have an inadequate communication by:

- not telling the truth on the transposition of the directive,

- not communicating on all the aspects of the issue involving the jurisdiction.

I am afraid the Irish regulator is worse in its communication on Madoff case than the Luxembourg regulator.

When going through the websites of the regulators (CSSF and IFS ) it appears that the IFS has a poor communication. The Irish Regulator communicated on Madoff the first time only a couple of weeks after the Luxembourg regulator.

The IFS issued only one laconic press release dated 7 January 2009 entitled “Bernard L Madoff Investment Securities LLC (“Madoff”) “ that does not quote the involved investment funds in Ireland : “Two funds, one UCITS and one non-UCITS, have exposures to Madoff arising from the appointment of Madoff as sub-custodian to the assets of the funds by the Irish trustee”

It is not the first time that I point out that the Luxembourg regulator is better that the Irish Regulator for the communication (see my article dated 14 October 2006).

A search on the website with the keyword Madoff confirms the feeling:

Search Results

• News (1)

• Remainder of site (1)

Both results are about the only press release dated 7 January.

Even though the CSSF communication in Luxembourg is not sufficient enough in a world of transparency, there is a communication that shows a minimum of respect for the investor:

11 February 2009: Withdrawal of the sicav HERALD (LUX) from the official list

6 February 2009: The Madoff case

6 February 2009: Meeting between UBS and the CSSF regarding the Madoff case

3 February 2009: Withdrawal of Luxalpha Sicav from the official list

23 January 2009: The Madoff case

2 January: The Madoff case

22 December 2008: Bernard L. Madoff and Bernard L. Madoff Investment Securities LLP

A search on the website with the keyword Madoff confirms the positive feeling with nine results.

I wish Luxembourg realised that it must target and fix dysfunctions and “red flags” that harm the Ethical credibility of the center and create the risk with periodic involvement of the jurisdiction.

07:50 Posted in Comparison | Permalink | Comments (0)

02/11/2009

Edhec report highlights Madoff red flags that should have been warning signals

In an excellent report François-Serge Lhabitant and Greg Gregoriou, from the Edhec Risk and Asset Management Research Centre, highlight some of the salient operational features common to best-of-breed hedge funds - features that were clearly missing from Madoff's operations.

The Edhec position paper looks at the events leading up to the fraud and considers how the alleged split-strike conversion strategy would have worked before exploring the due diligence aspects of the case in detail.

Among the areas which should have been seen as a concern, the authors say, were operational red flags and investment red flags

Operational red flags were :

- lack of segregation amongst service providers,

- obscure auditors,

- an unusual fee structure,

- heavy family influence,

- lack of disclosure,

- insufficient staff,

Investment red flags were :

- black-box strategy,

- questionable style exposures,

- incoherent 13F filings,

- excessive market size.

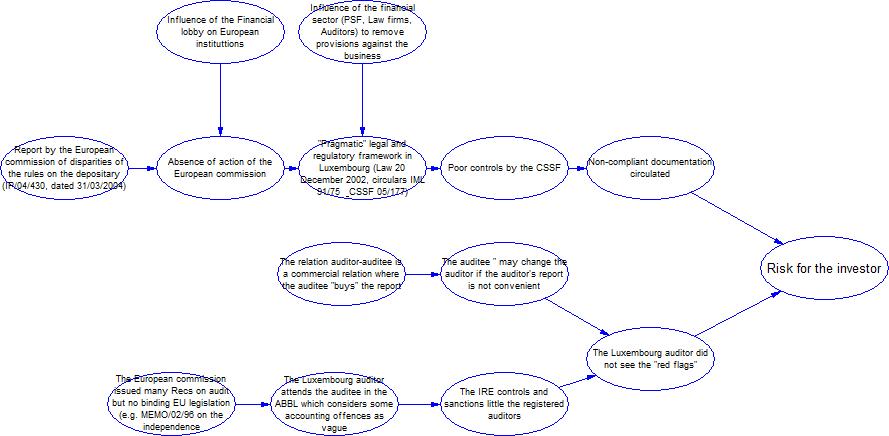

Most of the identified operational red flags are definitely met in luxembourg :

- lack of segregation amongst service providers,

- obscure auditors,

- heavy family influence,

- lack of disclosure,

- insufficient staff.

Read paper

05:30 Posted in General | Permalink | Comments (0)

02/08/2009

Latest Recast of the Directive 85/611/EEC: missing provisions in the Luxembourg law still required

The lastest proposed changes to the UCITS Directive dated July 2008 are intended to remove administrative barriers to the cross-border distribution of UCITS funds, create a framework for mergers between UCITS funds, allow the use of master-feeder structures, replace the Simplified Prospectus by a new concept of Key Investor Information and improve cooperation mechanisms between national supervisors.

I have pointed out two provisions of the Directive that was issued in 2005 that are missing in the Luxembourg law of transposition.

The question is: are these provisions still required after the changes to the UCITS framework?

The answer is definitely yes even though the number of the articles and the wording was changed.

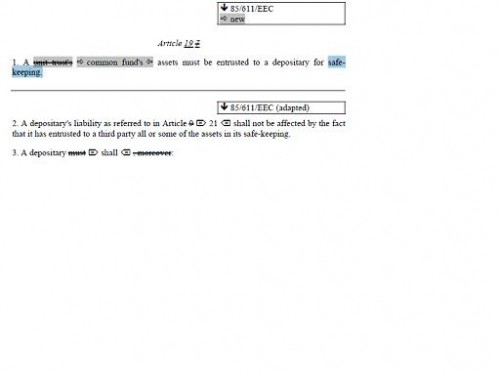

Article 7 is now article 19 with the following first paragraph: “1. A common fund's assets must be entrusted to a depositary for safekeeping”

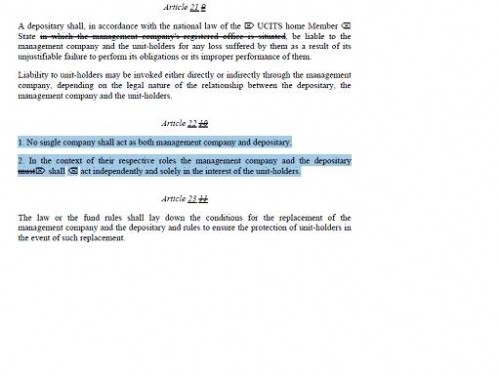

Article 10 is now article 22 with the following text: “1. No single company shall act as both management company and depositary. 2. In the context of their respective roles the management company and the depositary shall act independently and solely in the interest of the unit-holders.”

“Must act independently” was replaced by “shall act independently” for the second paragraph.

When officials in the Luxembourg jurisdiction dare to state that the Luxembourg law complies with the European Directive like the ALFI before the EFAMA: “Minister Luc Frieden and then Prime Minister Jean-Claude Juncker unequivocally stated that Luxembourg has faithfully transposed the UCITS Directive", it is definitely a stupid lie as very easy to check and politicians and professionals of the ALFI in the jurisdiction are no longer trustable.

This is true as well for AML provisions, anti bribery provisions… The Pandora box is opened.

When one does not tell the truth on something easy to check, he/she is no longer trustable and reliable in the business.

It is definitely worrying for the financial community worldwide whose success is based on confidence and that cannot support anymore a weak link.

That is the reason why I sent yesterday the following e-mail to Commissioner McCreevy:

Dear Mr Mc Creevy

The Luxembourg authorities state that the Luxembourg law to transpose the UCITS directive complies with the UCITS Directive.

I am afraid leaders of the financial center of Luxembourg are not telling the truth, which is all the more unacceptable than it is easy to check by building a synoptic table I have attached.

There are actually two critical provisions that are missing in the Luxembourg text but that can be found in the Irish text.

1)

Article 7 of the UCITS directive states that “1. A unit trust's assets must be entrusted to a depositary for safekeeping”. The word “safekeeping” was removed in the transposition (Cf. article 17 of the Luxembourg Law of 20 ecember 2002). Additionally, Circular IMS 91/75 (as amended by Circular CSSF 05/177) dated 21 January 1991 states that “The concept of custody used to describe the general mission of the depositary should be understood not in the sense of “safekeeping”, but in the sense of “supervision” (…) The depositary has discharged its duty of supervision when it is satisfied from the outset and during the whole of the duration of the contract that the third parties with which the assets of the UCI are on deposit are reputable and competent and have sufficient financial resources.“

2)

Article 10 of the UCIT directive states that “ 1. No single company shall act as both management company and depositary”. Such provision is not in the Luxembourg text. This first paragraph was removed to only transpose literally paragraph 2 that states that “2. In the context of their respective roles the management company and the depositary must act independently and solely in the interest of the unit-holders.” (Cf. article 20 of the Luxembourg law of 20 December 2002)

What is not prohibited by the law is possible and it seems that UBS acted both as Management Company and depositary.

ALFI’s views on the Madoff affair and its implications for the Luxembourg fund industry that was presented at the EFAMA Management Committee meeting held on Tuesday, 20 January was therefore a misleading communication. So is a misleading communication what stated the governmental authorities about the legal and regulatory framework of the jurisdiction.

In a nutshell, time is up for the Commission to smell the coffee and realise that by its feeling of impunity and of being above the law (they are not telling the truth publicly on things easy to verify), Luxembourg threatens the credibility of the ethical policies.

Best regards.

Jérôme Turquey

Consultant in Business Ethics and Reputational Risk

http://ethiquedesplaces.blogspirit.com

I am looking forward to reading his answer. If I get one as I do consider that the European Commission did not do its job and has a liability in the situation.

{kind=link}

By the way, who chairs the Eurogroup?

11:00 Posted in General | Permalink | Comments (1)