08/30/2009

Whistle blowing always leads to a dead end

In this blog I have expressed several times that I do not agree with whistle blowing despite it is promoted by international organizations like GRECO or OECD : whilst the OECD Convention on bribery does not impose specific obligations regarding whistle blowing the OECD monitoring procedures identify reporting mechanisms and whistle blower protection as relevant factors for detecting and deterring bribery.

Whistle blowing is based on internal information that is communicated and therefore is clearly a breach of loyalty. There are many public and official facts in the jurisdictions that allow to trace both a lax attitude and a support to professionals that do not comply with professional standing. I have decided to focus on these and I refuse any information that is not public or official I could be sent.

The definition of corruption is large enough to include those who organize huge banking schemes to facilitate tax evasion.

The UBS tax scandal in the USA started with Bradley Birkenfeld, who acted as a whistleblower. This guy was sent to jail for facilitating offshore tax evasion through UBS banking schemes, despite assisting federal investigators in exposing the secretive bank whereas it was agreed between the USA and UBS that UBS would disclose 4,450 client names instead of the 52000 targeted.

A couple of days later President Barack Obama played the golf with Robert Wolf, president of UBS Investment Bank and chairman and CEO of UBS Group Americas. Wolf, an early financial backer of Obama's presidential campaign, raised $250,000 for him back in 2006, and in February was appointed by the president to the White House's Economic Recovery Advisory Board.

There is all but an happy end for whistleblowers and I did not read any support for Bradley Birkenfeld from the OECD or the GRECO, those organizations that promote what he did.

I think these organisation are neither trustable nor reliable as they are upset when one reports red flags from public and official sources. So how can they actually support the reporting of information that is more confidential ?

07:22 Posted in General | Permalink | Comments (1)

08/23/2009

Luxembourg : the half-regulated center

Luxembourg is said to be a regulated and international financial center.

In the framework of my study to compare some jurisdictions with the view to inform investors and clients, I can’t help posting the findings that Luxembourg is actually for the least a half-regulated center.

I know that many professionals with business standing in the jurisdiction do not like criticism and that their immature reaction is to fustigate an unhealthy combination of gratuitous assertions, hearsay, half-truths and concocted lies instead of tightening up the ship whenever issues are raised.

So I will use official sources to point out the failures of the regulation.

1) Failure of the regulator to inform investors for their protection.

Should such failure be demonstrated it would be crippling and the Ad stating “Luxembourg: regulated and international financial center” would be misleading.

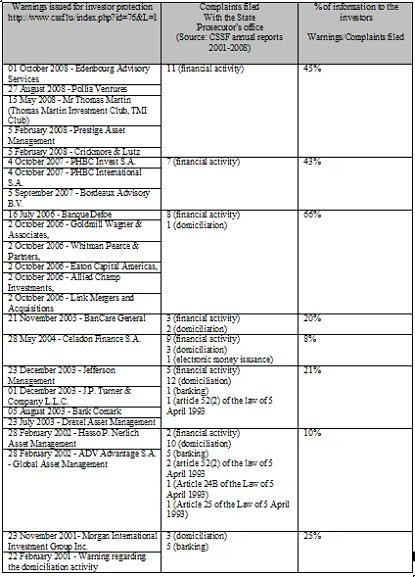

My sources are provided by the regulator, the CSSF itself: on the one hand warnings published by the CSSF regarding suspicious activities of certain companies (in the investor protection section) and on the other hand CSSF annual reports (in the Publications section).

Unfortunately as transparency is not the quality of the jurisdiction, annual reports do not specify the persons involved so it is not possible to verify if every warning triggered a complaint .

As the annual reports specify in the “Means of sanctions available to the CSSF” chapter (9th chapter currently), the CSSF informs the State Prosecutor of any instance of non-compliance with legal provisions relating to the financial sector, giving rise to penal sanctions and that could entail prosecution against the implicated persons. The following cases are concerned:

- persons performing an activity of the financial sector without holding a licence;

- persons active in the field of company domiciliation without belonging to any of the professions entitled by the law of 31 May 1999 governing the domiciliation of companies as amended to carry on this activity;

- persons other than those registered on the official lists of the CSSF, who use a title or appellation, thereby breaching Article 52(2) of the law of 5 April 1993 on the financial sector, as amended, that gives the appearance that they are authorised to perform one of the activities reserved for persons registered on one of the lists;

- attempted fraud

There should not be any discrepancy between warnings published by the CSSF regarding suspicious activities of certain companies and complaints filed with the State Prosecutor’s office.

Otherwise this would mean that practically the CSSF would not protect the investor in an appropriate way : in other words by not being informed in time of every case filed, investors might loose their money with some persons that the CSSF knew were dubious.

Let’s see (click to enlarge):

The figures are telling: the last two years (the “current” regulation) investors were not informed of 50% of complaints filed with the State Prosecutor’s office.

2) Failures of banks to report Suspicious Transaction reports

This symbolic percentage of 50% reminds me of the percentage of banks that never ever reported a declaration of suspicion according to the CRF, the Luxembourg FIU

According to the CRF, many banks never ever reported a Suspicious Transaction report. Practically half of the banks report a Suspicious Transaction reports. It is not possiblethat there isn’t at least one report.

Report 2008 page 15

La proportion des banques ayant opéré une ou plusieurs déclarations à la CRF est demeurée globalement stable depuis 2002 et représente environ la moitié des banques de la place.

Un examen statistique plus approfondi confirme le phénomène relevé dans les rapports d’activités antérieurs, à savoir qu’un faible nombre de banques représente la majorité des déclarations du secteur.

(…)

Il ressort de ce qui précède qu’un grand nombre de banques ne procède pas sinon très peu à des déclarations de soupçon.

NB: This report was not promoted by the government but the information was circulated by the ALCO

Report 2007 page 14

La proportion des banques ayant opéré une ou plusieurs déclarations à la CRF est demeurée globalement stable depuis 2002 et représente environ la moitié des banques de la place.

Un examen statistique plus approfondi confirme le fait qu’une large majorité des déclarations est effectuée par un nombre très restreint d’établissements de crédit (…)

Ainsi, comme constaté dans les rapports antérieurs, un grand nombre de banques ne procède pas sinon très peu à des déclarations de soupçon.

Les causes de ce phénomène n’ont pas été identifiées par la CRF qui ne dispose pas de compétence pour mener des contrôles sur place systématiques afin de vérifier le respect de leurs obligations professionnelles par les banques n’ayant pas déclaré de soupçon pendant l’année sous examen.

Report 2005-2006 pages 11-12

La proportion du nombre de banques ayant au moins opéré une déclaration de soupçon est demeurée stable depuis 2002 et représente environ la moitié des banques de la place. Cette constatation est cependant sensiblement relativisée par le fait qu’une large majorité des déclarations est effectuée par un nombre très restreint d’établissements de crédit.

Comme pour la période précédente, il y a partant lieu de relever qu’un grand nombre de banques ne procède pas sinon très peu à des déclarations de soupçon. Les causes de ce phénomène ne sont pas connues de la CRF.

Report 2003-2004 page 9

Il y a une certaine stabilisation du nombre de banques ayant opéré une ou plusieurs déclarations de soupçon. En effet, depuis 2002, environ la moitié des banques de la place a opéré au moins une déclaration d’opération suspecte auprès de la CRF par an.

Ce chiffre est cependant sensiblement relativisé par le fait qu’une large majorité des déclarations est effectuée par un nombre très restreint d’établissements de crédit (…)

Un grand nombre de banques ne procède pas sinon très peu à des déclarations de soupçon.

Report 2001-2002 page 12

L’évolution du nombre des établissements de crédit agréés

1998 : 209

1999 : 210

2000 : 202

2001 : 189

2002 : 177

L’évolution du nombre des établissements différents ayant opéré une ou plusieurs déclarations est la suivante :

1998: 32

1999: 36

2000: 31

2001: 59

2000 : 80

Le pourcentage d'établissements ayant opéré une ou plusieurs déclarations est le suivant :

1998 : 15%

1999 : 17%

2000 : 15%

2001 : 31%

2002 : 45%

Conclusion: This is the visible part of the iceberg because many data are not available to assess the quality of the regulation in every area as transparency is not a hallmark of the jurisdiction. But the figures are telling enough to conclude that the communication about the regulated center is deceptive. Definitely deceptive for clients as well as for international organisations (OECD, FATF, IMF…).

06:40 Posted in Luxembourg | Permalink | Comments (0)

08/22/2009

Poor Regulation for a poor protection for clients

Last year, on 15 May 2008, the Commission de Surveillance du Secteur Financier warned the public of the activities of a certain Mr Thomas Martin acting notably under the name “Thomas Martin Investment Club” and “TMI Club” (address: 34, parc Syrdall, L-5365 Munsbach).

According to the information available to the CSSF, the above-mentioned person offered services of the financial sector.

The Commission de Surveillance du Secteur Financier informed the public that neither Mr Thomas Martin, nor “Thomas Martin Investment Club”, respectively “TMI Club” had been granted the required authorisation to offer such services in or from Luxembourg.

The information was circulated as well by the Centre Européen des Consommateurs. But only the CSSF and the Centre Européen des Consommateurs circulated the information.

A couple of days before the warning Thomas Martin was interviewed and he presented himself. The conversation took place online NOT face to face.

1.) Hi Admin, where do you come from?

I am a retired man from Western Europe, I am more precisely French but lived in Switzerland and Luxembourg most of my life. I am what people call a self-made-man, didn’t study a lot as I had to work quickly, so I had many and various jobs. Finally I ran a small HR Cabinet in Switzerland, where I met a lot of high executives in the financial world. They opened my eyes and my mind to finance, and all began really.

2.) Why did you decided to start an online investing program?

Well to be frank I didn’t decide by myself to go online. In 1990 I opened a very small and very private Club, where a few friends and I invested our hard earned money. Years after years the Club grew, without any other advertising than private conversations.

Then a few years ago my son Stan joined me, it was if I remember around the year 2000. As he is from another – younger! – generation, he was very opened on the internet world, and began to say “why not go online”! I wasn’t very happy of this as our success was, in my opinion, due to our private and confidential status. But years after years he convinced me and in 2007 we decided to offer our online program.

The rule is simple: Higher is the amount of our funds, more we invest and more we make profit. So, why not coming online, despite I must confess that after what I saw on the internet, I was not very enthusiast to open a website. The danger for him was the Club to be mixed with all “ponzi” that are around.

Finally so we hired a programmer to write our software, and came online!

3.) So how long has your program started?

So, our program – the Club – was launched in 1990, and we came online in 2007. It will soon be one year we are online.

4.) What type of payment processors do you accept and do you plan to accept more payment processors in the future?

Most of our business is made through bank wires. But we understood that coming online, we will need to accept e-currencies. According to Stan, the most popular was e-gold, the most serious e-bullion, so we decided to accept them.

Later we added Libertyreserve, but we will probably remove it if they do not fix their problems really quickly, I suppose you know their situation!

We are opened to new processors, but as far as I can see, there is nothing serious now! Let’s wait, maybe something really new and great will come? Nevertheless once more, the best way to work with us is using bank wires.

5.) How confident are you with your site security level?

Sorry we do not communicate about this topic.

6.) What are your plans for the future and how long do you think you will stay online?

We have no plans to not stay online! Do you think that any company can think “when will we close?”? Our program works, and worked since 1990!

We turned into a registered company last month. We are expecting to receive a bank license next year; we will emit our payment cards (OUR cards and not third party cards), offer certificates of deposit and other bank services. As you see, our plans for the future look fine!

7.) Do you have any phone support other than email support?

Yes we have but only on a case by case basis, as Stan (he cares of the Support) has really no time to return phone calls. Support is now done through a “ticket center” that allow our Investors and us to keep a trace of all exchanges.

I add that I sometimes meet some Investors or potential serious Investors, but as I am very often travelling it isn’t that easy. Our commercial director, Alain Martel, meets more frequently people, especially in Europe.

8.) Can you explain on how you calculate the ROI of your plan?

We offer 10.25% by month. This is an average return we can pay, we of course do not exactly make 10.25% every month. We can for example make 50% one month (we made even more some times!), then a month in loss, etc. Globally with paying 10.25% to our Investors, believe me we still have some nice profit for us!

9.) Do you have a physical office/address for your program/company?

We have a small office in Luxembourg but we do not disclose the place, anyway we will close it as we have now no more link with Luxembourg. When we need to meet people, we find a place: At home sometimes, or we rent an office in a business center, or in a good restaurant!

10.) How many percentage of the funds received from investor will go to admin, staff profit?

None. We invest 100% of the funds we receive. We make our living on the profit we generate, not on the funds we receive.

11.) Lastly in less than 50 words, briefly describe what can your program give to your investors?

A High, Regular and Honest Income! High as 10.25% is really high, Regular as we pay this rate or just about this rate since 1990 without any break, Honest because we do not invest in illegal activities, AND we do not pay Investors with the investments of others!

Thomas Martin’s website does not exit anymore and many investors are saying he left with their money and have filed a complaint.

This story raises one question: Why it was so long for the Luxembourg regulator to warn clients: the business was created as of 1990 and the warning was published 18 years later?

Luxembourg is a small jurisdiction where everybody knows everyone and what the others are doing.

The activity should have been detected earlier. Information on the business had circulated on the internet at least since October 2007.

There were many red flags:

In the 2000s there is no business in the investment activity that does not have a website.

Additionaly, the address was a PO Box. The so-called phone number +1.8318506188 that seems from California is from Pac-West Telecom California. PacWest provides notably VoIP services.

Finally, Thomas Martins seems to be located now in the Seychelles. The telephone is still the one of Luxembourg and the fax is the so-called phone number from California.

In the context of the Luxalpha affair, this story that is not circulated in Luxembourg (the Keydata affair is not circulated either), demonstrates that the regulation is at the very least perfectible.

08:38 Posted in Luxembourg | Permalink | Comments (0)