06/05/2009

Switzerland is losing the capital of credibility that I gave it

Le temps has reported that Switzerland is willing to introduce specific provisions in the tax agreements that are to be signed.

- On the one hand, the request of the foreign jurisdiction would describe the behaviour in question, the name of the author, as well as the documents on which the jurisdiction bases its suspicions. If the foreign authority seeks to make raise the bank secrecy protecting the author from supposed tax evasion, the name of the Swiss bank should also be indicated in the request. This requirement of precision aims at preventing fishing with information by foreign tax authorities.

- On the other hand, Switzerland should negotiate the way in which the foreign jurisdiction can collect evidence to refuse requests that are based on evidence on an unlawful basis, according to the Swiss law.

I know that there is a change in progress in Luxembourg. Not with the LIGFI which is an association of the past as it is promoted by leaders of the jurisdictions that never ever repudiated, at least publicly, drifts and abuses in Luxembourg. It is about a major change which transcends the parties. The stake is to substitute the best elements for an old guard.

06:09 Posted in Switzerland | Permalink | Comments (0)

06/04/2009

France and Luxembourg: the respective misleading agreement

Luxembourg signed a tax agreement on the OECD tax model with France to improve its image.

I am afraid this will not hush up litigious issues at is seems that they did not sign up for the same purpose.

Let’s have a look on their respective press release:

The French press release states that: “les dispositions de cet article permettront à la France d’obtenir des renseignements sans limitation quant à la nature des impôts, des personnes et des renseignements visés par la demande de renseignements. Ces demandes de renseignements pourront ainsi désormais porter sur des renseignements bancaires sans que la législation interne luxembourgeoise puisse y faire obstacle (...) La signature de cet avenant contribue à la lutte contre la fraude et l’évasion fiscales, puisqu’il permet désormais à la France d’obtenir des renseignements de la part des autorités luxembourgeoises sans limitation quant à la nature des impôts, des personnes et des renseignements visés par la demande de renseignements. »

(free translation: the provisions of this article will make it possible for France to obtain information without limitation relating to the nature of the taxes, the people and the information targeted by the request for information. These requests for information will be able from as of now to be about banking information without the Luxembourg national legislation being opposable to it (...) the signature of this endorsement contributes to the fight against fraud and tax evasion, since it makes it possible as of now for France to obtain information from the Luxembourg authorities without limitation as for the nature of the taxes, the people and the information aimed at by the request for information.”)

The Luxembourg press release states that: « Le protocole prévoit l'échange d'informations sur demande dans des cas individuels entre les administrations fiscales des deux pays. Il s’applique aux années fiscales 2010 et suivantes. L’accord n’a pas pour objet un échange automatique d’informations bancaires et n’autorise pas des demandes générales (fishing expeditions)."

(free translation: “The protocol envisages the information exchange on request in individual cases between the tax authorities of both countries. It applies to the financial years 2010 and following. The agreement does not have as an aim an automatic exchange of banking information and does not authorize general requests (fishing expeditions).”)

While Luxembourg does want neither the automatic exchange of banking information nor fishing expeditions, France believes that it will get “without limitation” (“information without limitation relating to nature of the taxes, the people and the information aimed at by the request for information “ is repeated twice in the press release) information on any taxpayer (its taxes, its bank accounts…).

What a charade.

17:30 Posted in Luxembourg | Permalink | Comments (3)

06/01/2009

Pragmatism of deposit-guarantee schemes in Luxembourg

Directive 2009/14/EC of the European Parliament and of the Council was transposed in le Luxembourg legislation.

Luxembourg clear and pragmatic transposition of European directives is visible once more. Lucien Thiel was rapporteur of the law. He is one of the founders of the LIGFI.

The minimum coverage is not clearly increased as it appears that there is no budget to do so.

Additionally the wording of the transposition of one of the clauses of the directive is interesting.

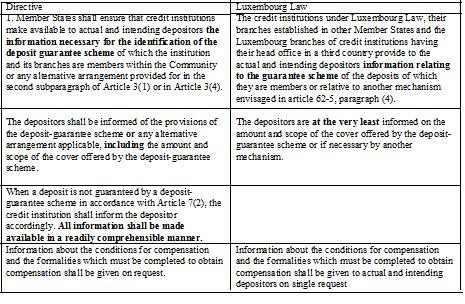

The directive states that “1. Member States shall ensure that credit institutions make available to actual and intending depositors the information necessary for the identification of the deposit guarantee scheme of which the institution and its branches are members within the Community or any alternative arrangement provided for in the second subparagraph of Article 3(1) or in Article 3(4). The depositors shall be informed of the provisions of the deposit-guarantee scheme or any alternative arrangement applicable, including the amount and scope of the cover offered by the deposit-guarantee scheme. When a deposit is not guaranteed by a deposit-guarantee scheme in accordance with Article 7(2), the credit institution shall inform the depositor accordingly. All information shall be made available in a readily comprehensible manner.

Information about the conditions for compensation and the formalities which must be completed to obtain compensation shall be given on request”

The Luxembourg law states that « (1) Les établissements de crédit de droit luxembourgeois, leurs succursales établies dans d’autres Etats membres et les succursales luxembourgeoises d’établissements de crédit ayant leur siège social dans un pays tiers fournissent aux déposants effectifs et potentiels des informations relatives au système de garantie des dépôts dont ils sont membres ou relatives à un autre mécanisme prévu à l’article 62-5, paragraphe (4). Les déposants sont pour le moins informés sur le montant et l’étendue de la couverture offerte par le système de garantie ou le cas échéant par un autre mécanisme. Des informations relatives aux conditions d’indemnisation et les formalités à remplir pour être indemnisés sont fournies aux déposants effectifs et potentiels sur simple demande »

Free translation : “The credit institutions under Luxembourg Law, their branches established in other Member States and the Luxembourg branches of credit institutions having their head office in a third country provide to the effective and potential depositors information relating to the guarantee scheme of the deposits of which they are members or relative to another mechanism envisaged in article 62-5, paragraph (4). The depositors are at the very least informed on the amount and scope of the cover offered by the deposit-guarantee scheme or if necessary by another mechanism. Information about the conditions for compensation and the formalities which must be completed to obtain compensation shall be given to actual and intending depositors on request”

Synoptic table :

The wording of the directive is changed, which opens the drift for a misleading communication:

- If the directive requires to provide “to actual and intending depositors the information necessary for the identification of the deposit guarantee scheme ”, the Luxembourg text states " to actual and intending depositors information relating to the guarantee scheme". The wording of the requirements is vague: "the information necessary" v. "information relating"

- If the directive requires that “depositors shall be informed of the provisions of the deposit-guarantee scheme or any alternative arrangement applicable, including the amount and scope of the cover offered by the deposit-guarantee scheme” the Luxembourg law only requires "at the very least" the amount and scope of the cover offered : the impact is not the same. Information that must be provided is larger in the directive.

- The provision of the directive “When a deposit is not guaranteed by a deposit-guarantee scheme in accordance with Article 7(2), the credit institution shall inform the depositor accordingly. All information shall be made available in a readily comprehensible manner” is not in the Luxembourg text.

These are facts of a misleading information that will be provided knowingly to the investor on deposit-guarantee schemes in Luxembourg: I am afraid the transposition does not comply with the principles of integrity, as stated by Jacques Santer for the launch of the LIGFI: transparency, fairness, responsibility and accountability in the financial sector.

This reminds me of the pragmatic transposition of the UCITS directive that opened the drift with Madoff, which is denied but definitely proven with a synoptic table.

18:51 Posted in Luxembourg | Permalink | Comments (1)