07/21/2012

OLOS and the regulation

In my previous post, I mentioned my investigation in the Luxembourg Corporate registration about a businessman named Flavio Becca: I did not know him and had never heard about him.

I found that he was founder and/or director of 84 companies.

I found as well that he became a PSF (Professional of the Financial Sector), regulated by CSSF with the creation of LYNX INVESTMENT MANAGEMENT S.A. that was later renamed OLOS MANAGEMENT S.A, and of a fund linked to it, which resulted from the merger of many of Becca’s companies to build the fund.

The analysis of every publication relating to LYNX/OLOS is very interesting.

Members of the Board were originally

a) Mr Jean-Claude FINCK, General Manager and Chairman of BCEE

b) Mr André WILWERT

c) Mr Flavio BECCA

d) Mr Eric LUX

e) Mr Romain BONTEMPS

When the study was published late September 2011, Mouvement Ecologique emphasized that Jean-Claude FINCK, who is first quoted on the list, should not be there. And Finck resigned a couple of weeks later. He actually should never have been involved in such a venture.PwC is the auditor of the fund.

The press reported (French or German) that according to the last audit reports, it appears that Flavio Becca's fund OLOS is sitting on a mountain of mortgages that total €508 million. Usually such a heavy load of mortgages is not an issue, but should real estate lose value, the fund could get into financial trouble.

Most experts expect Luxembourg's real estate market to continue to be stable despite the present economic crisis that cannot be hidden anymore. The threat of a real estate bubble does not exist, according to the same experts who denied that the center was perfectible in its regulation. But then got a huge surprise after the publication of a very negative FATF (Financial Action Task Force of OECD) report.

The prices for real estate are rather climbing. Still Becca's investments can only be profitable if he doesn't sell in the short term, according to PwC.

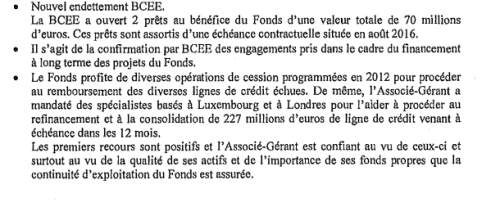

However in their analysis PwC notes that credits of €227 million must be paid back next year. The fund has ordered "specialists in London and Luxembourg" to find a solution to pay them back, which probably can only be done by refinancing and restructuring the debt Will there be any takers?

According to the media, the manager of the fund is "confident" that the continuing existence of the fund is secured, according to the report.

However, according to RTL that quoted Land, "La trésorerie de Flavio Becca est ex-sangue et ses banquiers ne sont plus disposés à lui ouvrir le robinet des crédits, notamment pour alimenter le fonds OLOS, regroupant notamment les participations immobilières de Flavo Becca et ne valant plus rien." (Free translation “Flavio Becca's finance is pale and bankers are no longer inclined to open him the credit faucet, in particular to feed the fund OLOS, merging in particular the Flavio Becca’s real estate participations which are basically worthless.”)

And Land quoted by RTL to underline that « Selon des informations du Lëtzebuerger Land, il faut que les juristes de la BCEE soient consultés quand les lignes de crédits du fonds sont augmentées » (free translation : According to information from Lëtzebuerger Land, lawyers of BCEE have to be consulted when credit lines of the funds are increased)

Finck resigned on 25 November 2011. He was definitely director most of the year under review (328 days) in a company where the bank he chairs is a stakeholder.

The last page of the audit report is very interesting

It says “new debts towards BCEE”, which means that there are already debts that were contracted when Finck was director.

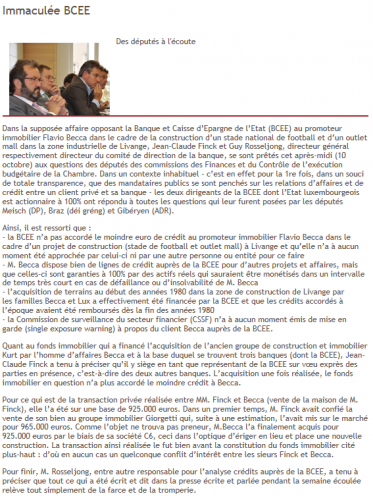

In this context it is amazing to read again a publication online on the website of Chambre des Députés : “Immaculate BCEE”

« M. Becca dispose bien de lignes de crédit auprès de la BCEE pour d’autres projets et affaires, mais celles-ci sont garanties à 100% par des actifs réels qui sauraient être monétisés dans un intervalle de temps très court en cas de défaillance ou d’insolvabilité de M. Becca (…) La Commission de surveillance du secteur financier (CSSF) n’a à aucun moment émis de mise en garde (single exposure warning) à propos du client Becca auprès de la BCEE (…) Jean-Claude Finck a tenu à préciser qu’il y siège en tant que représentant de la BCEE sur vœu exprès des parties en présence, c’est-à-dire des deux autres banques. L’acquisition une fois réalisée, le fonds immobilier en question n’a plus accordé le moindre crédit à Becca »

(free translation : Mr. Becca actually has credit lines with BCEE for other projects and businesses, but these are guaranteed to 100% by actual assets which could be monetized in a a very short time in the event of failure or of insolvency of Mr. Becca (…) CSSF never ever issued any single exposure warning relating to Becca, client at the BCEE (…) Jean-Claude Finck made a point of specifying that he is a Board member there as a representative of BCEE on the express wish of the parties, i.e. of the two other banks. The acquisition once carried out, the real estate fund in question did not grant the least credit any more to Becca.

The real estate fund in question did not grant the least credit any more to Becca. Until recently…

It is not clear either what BCEE's total exposure to Becca is. There is the information about 2 loans totaling € 70 million. And then there are credit lines not further specified. But PwC mentions that in order to draw any further on those credit lines, BCEE's lawyers have to be informed. Does this mean that BCEE should or will actually cancel those credit lines, but maintains them as window dressing so the auditors and potential new investors remain comfortable? Does it mean that BCEE took precautions to pull the plug in the event of a further deterioration of cash flow?

I also thought about Moody's and there comment that 43% of Luxembourg mortgages are issued by BCEE. If Becca falls, the bubble might burst, and many mortgages will be threatened. For the simple reason that people will have more residual debt than their real estate is worth. As happens in Spain, Greece, and the US where they call those mortgages "under water". that threat, though remote, has been factored into Moody's downgrade of BCEE.

Data relating to the fund are available on Finesti

OLOS Accounts are online on Fisec blog

17:00 Posted in Luxembourg | Permalink | Comments (2)

Comments

Bravo pour cet excellent billet. Le sujet ma toujours interesse aussi et je doit admettre que celui-ci est une reference.

Au plaisir.

Posted by: gagner plus d argent | 05/20/2013

fabuleux article, merci bien.

Posted by: Courtier immobilier | 01/04/2015

The comments are closed.