03/07/2009

Banking secrecy and the levels of permissiveness

Luxembourg, Switzerland and Austria are to meet this week end in Luxembourg.

The meeting will take place in Luxembourg and will serve primarily to coordinate points of common interest of the financial centres in the international environment. The talks will cover a range of issues including the debate surrounding a possible blacklist of so-called `tax havens'

Even though Luxembourg, Switzerland and Austria share banking secrecy, by comming in Luxembourg Switzerland and Austria are unfortunately supporting a jurisdiction that does not have the same level of business ethics than them, which weakens the legitimacy of their arguments.

By acting like this they encourage Luxembourg to refuse the brushing up of the country toward ethics and good governance.

Let's compare the three jurisdictions on a couple of items :

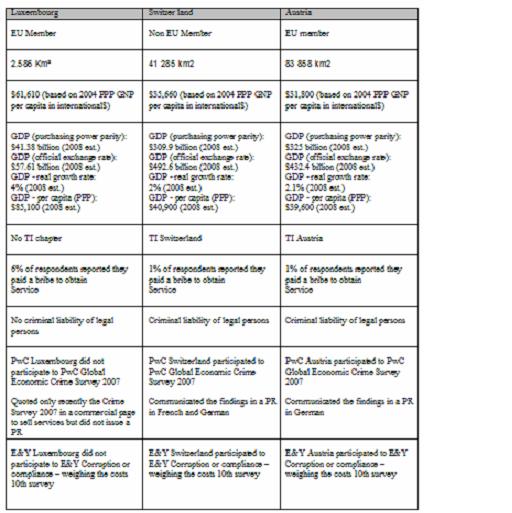

Size

Luxembourg : 2.586 Km²

Switzerland : 41 285 km2

Austria : 83 858 km2

Luxembourg is the smallest jurisdiction of the three, which means a jurisdiction where everybody knows everyone with a high level of conflicts of interests.

GNP per capita in international$ (Source : World's Richest Countries in Gross National Product - Daniel Workman)

GNP per capita based on global purchasing power parity (PPP). GNP per capita based on PPP represents the statistic converted to international dollars using purchasing power parity rates.

Luxembourg : $61,610 (based on 2004 PPP GNP per capita in international$)

Switzerland : $35,660 (based on 2004 PPP GNP per capita in international$)

$31,800 (based on 2004 PPP GNP per capita in international$)

Luxembourg is the richest jurisdiction of the three.

GDP (Source : CIA World Factbook)

Luxembourg : GDP - per capita (PPP): $85,100 (2008 est.)

Switzerland : GDP - per capita (PPP): $40,900 (2008 est.)

Austria: GDP - per capita (PPP): $39,600 (2008 est.)

Luxembourg is the richest jurisdiction of the three.

Transparency International Chapter (Source : TI Website)

Luxembourg: no chapter

Switzerland: TI Switzerland, located Schanzeneckstrasse 25, P.O. Box 8509, CH-3001 Bern. Contact Person(s): Ms Anne Schwöbel

Austria: TI Austria, located Operngasse 20B/9, 1040 Wien. Contact Person(s): Dr. Eva Geiblinger

Luxembourg that is the richest jurisdiction of the three, which means that has more opportunities for corruption and fraud because of conflicts of interests, does not have a TI Chapter.

Transparency International Global Corruption Barometer 2007 (Source : Report)

Luxembourg: 6% of respondents reported they paid a bribe to obtain Service

Switzerland: 1% of respondents reported they paid a bribe to obtain Service

Austria: 1% of respondents reported they paid a bribe to obtain Service

Luxembourg that is the richest jurisdiction of the three that does not have a TI Chapter is the one where more respondents reported they paid a bribe to obtain Service.

Liability of legal persons (Source : OECD and GRECO reports on corruption)

Luxembourg: "“Luxembourg has still not responded to key Phases 1 and 2 recommendations; these recommendations relate to the establishment of a clear, effective and dissuasive system of liability of legal persons and efforts to raise awareness of the foreign bribery offence among the private sector. Considering the seriousness of the situation, the Working Group has decided that, within one year, Luxembourg will report,in writing, on measures taken to fulfil the recommendations of the Group, and reserves the right, in the event of continued failure to implement the Convention, to take further steps.” (Source: OCDE Working Group on Bribery, Phase 2 bis, 20 March 2008, p. 4)

Switzerland: “Article 100quater of the Criminal Code institutes two systems of criminal liability for enterprises. Both establish defective organisation as a condition for corporate criminal liability.” (Source: OCDE Working Group on Bribery, Phase 2, 20 December 2004, p. 36)

Austria: “In October 2005, shortly after the Phase 2 on-site visit, the Austrian Parliament adopted legislation establishing general criminal liability of legal persons, including for bribery offences.” (Source: OCDE Working Group on Bribery, Phase 2: Report on Implementation of the OECD Anti-Bribery Convention, 16 February 2006, p. 4)

Luxembourg that is the richest jurisdiction of the three, which means that has more opportunities for corruption and fraud because of conflicts of interests, does not have a liability for legal persons.

PwC Global Economic Crime Survey 2007 (Source : Survey 2007, p. 40)

Luxembourg: PwC Luxembourg did not participate to the survey.

Switzerland: PwC Switzerland participated to the survey

Austria: PwC Austria participated to the survey

PwC Luxembourg that is located in the richest jurisdiction of the three, which means that has more opportunities for corruption and fraud, did not participate to the survey

Luxembourg: No press release on the Surveys but a commercial webpage quoting the Survey 2007 to sell PwC services

Switzerland: Issued a press release on the Survey 2007 in French and German

Austria: Issued a press release on the Survey 2007 in German.

Luxembourg:

Switzerland:

Austria:

PwC Luxembourg that is located in the richest jurisdiction of the three, which means that has more opportunities for corruption and fraud because everybody knows everyone, did not communicate either on previous Economic Crime Surveys contrary to the colleagues in Switzerland and Austria. They communicated on the Survey in a commercial web page to sell their services the first time for the Global Economic Crime Survey 2007.

E&Y Corruption or compliance – weighing the costs 10th survey (Source: Survey page 23)

Luxembourg: E&Y Luxembourg did not participate to the survey.

Switzerland: E&Y Switzerland participated to the survey

Austria: E&Y Austria participated to the survey

E&Y Luxembourg that is located in the richest jurisdiction of the three, which means that has more opportunities for corruption and fraud, did not participate to the survey

There are more criteria but the above may be summarised on a synoptic table :

Large picture

{kind=link}

This comparison demonstrates that there is a scale of permissiveness in the jurisdictions. This is the reason why the Narcotic Control Strategy Reports 2008 observes “the scarce number of financial crime cases is of concern, particularly for a country that has such a large financial sector” or the the GRECO report Round III observes that “the number of cases coming before the courts appears to be very small”

This permissiveness increases more or less the negative effect of secrecy. There are recurrent scandals through Luxembourg: scams, tax evasion… Luxembourg clear and pragmatic framework is actually used to commit various frauds and ML cases.

E.g.

Fraud vis-à-vis the USA

Cipriani

Fraud with Liechtenstein

Fraud vis-à-vis France

Eurolux Gestion

AOL

Fraud vis-à-vis Italy

Consorte

Parmalat

Fraud vis-à-vis Spain

Esperito Santo with a sumary in English

Did professionals in the jurisdiction of 2500 Km2 where everybody knows everyone and what the others are doing realise the paradigm shift after the Liechtenstein scandal? As far as tax evasion is concerned I am afraid not as their behaviour demonstrates that in Luxembourg, secrecy is first a tool for fraud and obstruction to justice and tax administrations.

10:00 Posted in Comparison | Permalink | Comments (0)

03/05/2009

UBS made to disclose Luxembourg documents

Reuters has reported that a Luxembourg court ordered Swiss bank UBS to disclose some confidential documents within eight days or face a fine of 250 euros ($313.40) per day up to a maximum of 250,000 euros.

May be UBS will appeal the Luxembourg court order, like in the Oddo order case.

18:28 Posted in Luxembourg | Permalink | Comments (0)

New Legislation Would Combat Tax Haven Abuse, Increase Transparency, Accountability

As observes Global Financial Integrity, The introduction last Monday of The Stop Tax Haven Abuse Act, which would “restrict the use of offshore tax havens and abusive tax shelters to inappropriately avoid Federal taxation” by Senator Carl Levin (D-MI) represents a crucial step towards improving U.S. tax assessment and collection and strengthening the global financial system.

The Stop Tax Haven Abuse Act is similar to a previous bill, S. 681, introduced by Senator Levin in 2007 and cosponsored by then-Senator Barack Obama with 3 significant new additions that would:

(1) treat foreign corporations managed and controlled in the United States as domestic corporations for income tax purposes;

(2) close an offshore tax dividend loophole that enables offshore hedge funds and others to dodge payment of U.S. taxes on U.S. stock dividends; and

(3) expand the tax return reporting requirements for passive foreign investment corporations (PFICs) to include U.S. persons who don’t own a PFIC, but have formed, sent assets to, received assets from, or benefitted from a PFIC.

The jurisdictions that are considered as tax havens are :

Anguilla

Antigua and Barbuda

Aruba

Bahamas

Barbados

Belize

Bermuda

British Virgin Islands

Cayman Islands

Cook Islands

Costa Rica

Cyprus

Dominica

Gibraltar

Grenada

Guernsey/Sark/Alderney

Hong Kong

Isle of Man

Jersey

Latvia

Liechtenstein

Luxembourg

Malta

Nauru

Netherlands Antilles

Panama

Samoa

Singapore

St. Kitts and Nevis

St. Lucia

St. Vincent & the Grenadines

Switzerland

Turks and Caicos

Vanuatu

Delaware is missing.

The bill:

• Establish presumptions for entities and transactions in Offshore Secrecy Jurisdictions.

• Determine “Offshore Secrecy Jurisdictions.”

• Authorize special measures against foreign jurisdictions, financial institutions, and others that impede U.S. tax enforcement.

• Treat foreign corporations managed and controlled in the United States as domestic corporations for income tax purposes;

• Allow more time for investigations involving Offshore Secrecy Jurisdictions;

• Increase disclosure of offshore accounts, transactions, and entities;

• Prevent misuse of foreign trusts for tax evasion;

• Limit legal opinion protection from penalties with respect to transactions involving Offshore Secrecy Jurisdictions;

• Close the offshore dividend tax loophole;

• Increase penalty for failing to disclose offshore holdings;

• Require anti-money laundering rule for hedge funds;

• Apply anti-money laundering obligations to company formation agents;

• Strengthen John Doe summons use in offshore tax cases;

• Strengthen foreign financial account reporting requirements;

• Strengthen tax shelter penalties;

• Deter financial institution participation in abusive tax shelter activities;

• Strengthen law enforcement through information sharing;

• Require tougher tax shelter opinion standards for tax practitioners

“This is a pivotal time in global finance,” said Baker. “From the European Commission’s recent adoption of measures to improve cooperation between EU member states and increase transparency in tax assessment and collection to the G-20’s stated intent to crack down on tax havens when they meet in April, calls around the world are growing for definitive action on the problem of tax havens. This bill will ensure parity in U.S. tax remittance while strengthening overall global finance by increasing transparency and accountability.”

Stop Tax Haven Abuse Act : Summary

Stop Tax Haven Abuse Act (full text)

18:07 Posted in General | Permalink | Comments (0)