01/31/2009

Wooden language of the ALFI : Luxembourg unfortunately not a credible and reliable partner

The ALFI published last 29 January on its website the document giving ALFI’s views on the Madoff affair and its implications for the Luxembourg fund industry that was presented at the EFAMA Management Committee meeting held on Tuesday, 20 January.

The text is pure Luxembourg wooden language and unfortunately corroborate that leaders in the financial center of Luxembourg are far away from what is to be done prisoners of there insulated business culture.

Let's comment a few paragraphs :

Luxembourg regulation on the responsibility the depositary of an investment fund complies with the UCITS Directive and is equivalent to regulation in France

It is not true. Let’s compare the European directive with the Law of transposition dated 20 December 2002.

There is one critical provision that seems to be missing in the Luxembourg text.

Article 10 of the UCIT directive states that “ 1. No single company shall act as both management company and depositary”. Such provision is not in the Luxembourg text.

Paragraph one of Article 10 the UCIT directive was purely removed to only transpose literally paragraph 2 that states that “2. In the context of their respective roles the management company and the depositary must act independently and solely in the interest of the unit-holders.”.

What is not prohibited by the law is possible. When one knows that Luxembourg is a small jurisdiction where there are many conflicts of interests, requiring acting independently and solely with no requirement of being distinct legal entities is a beginning of problem. It is exactly like the law firm in Luxembourg that is both UBS and HSBC’s lawyers and provides the Chairman of the ALFI.

I will quote again Circular IMS 91/75 (as amended by Circular CSSF 05/177) dated 21 January 1991 that states that “The concept of custody used to describe the general mission of the depositary should be understood not in the sense of “safekeeping”, but in the sense of “supervision” (…) The depositary has discharged its duty of supervision when it is satisfied from the outset and during the whole of the duration of the contract that the third parties with which the assets of the UCI are on deposit are reputable and competent and have sufficient financial resources. “

Additionally the ALFI states that Luxembourg regulation on the responsibility the equivalent to regulation in France. I am afraid this is not true. As far as the provision Luxembourg removed is concerned France has transposed it with a rephrasing. Art. L. 214-16. of the French UCIT Code states that « Les actifs de la SICAV sont conservés par un dépositaire unique distinct de cette société et choisi sur une liste de personnes morales arrêtée par le ministre chargé de l'économie » (free translation : "The assets of the UCIT are preserved by depositary distinct from this [management] company and chosen on a list of legal persons stopped by the minister in charge for the economy")

The Luxembourg government and the country’s applicable regulatory and supervisory bodies acted as soon as the scandal broke to analyse and manage the consequences of the Madoff affair

The French regulator issued its first press release on 17 December 2008.

The Luxembourg regulator issued its first press release on 22 December 2008, 5 days later.

Additionally the French regulator issued on 18 December 2008 pedagogic material to explain the situation.

The first court ruling in Europe concerning the Madoff affair was given by a court in Luxembourg and was in the interests of investor protection

It is true. But the ALFI admits itself infra page 3 that “the legal basis in this specific case does not apply to all investors (ODDO had asked to redeem its shares before the fraud was uncovered).”

Luxembourg is in favour of a constructive process of reflection on investor safety in Europe and would like to see a debate based on an objective analysis of the situation

It is exactly like for other topics: for banking secrecy, for AML… Luxembourg always supports any a constructive process of reflection in Europe, which is mean to save time.

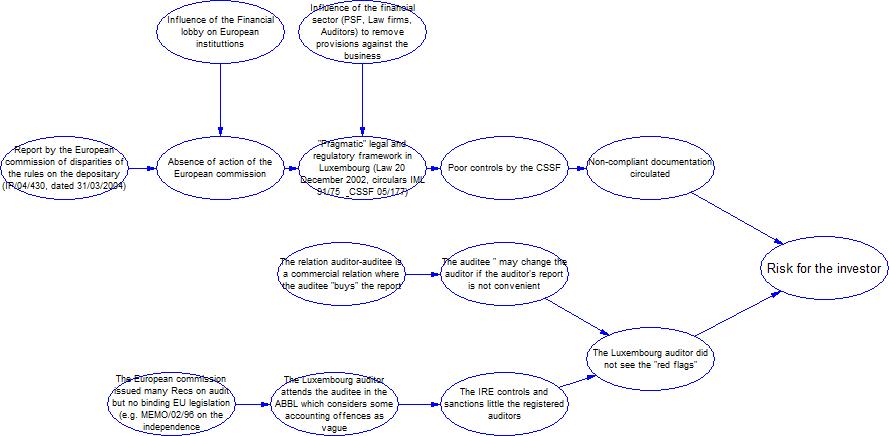

The objective situation is clear enough and may be summarized by a Fault Tree Analysis.

Large picture

{kind=link}

I am afraid those that are responsible for investigating the issue (the European Commission and the Luxembourg regulator) are part of the problem and not of the solution.

The letter [of Ms Lagarde] has also met with a very muted reception both from sector professionals and investors affected by the Madoff affair because it casts doubt on the effectiveness and even the existence of investor protection measures currently in place under European law. There is a real danger that this declaration of uncertainty could continue to shake the confidence of investors in Europe (and the world) in the UCITS brand.

At the same time, we wish to congratulate the Commission for opening an inquiry on the transposition of the UCITS Directive in various countries of the EU because it will answer the French criticisms of Luxembourg in this case.

The letter will certainly re-open the debate on European harmonisation of rules concerning fund depositaries. This is nothing new and has already been covered by a European Commission report in 2004. ALFI welcomes with interest this re-examination of current regulation and believes the first question to be asked should be what the status of the depositary is. Depositories in Luxembourg must be banks.

The first paragraph is the typical Luxembourg attitude when there are issues or dysfunctions. There is the will to hush up issues in the name of making money instead of tighten up the ship.

Such attitude is no longer acceptable all the more than despite a reassuring speech the transposition of the UCIT Directive in Luxembourg is lax and the European commission did not do its job.

This is by the way what stated the ALFI at the end by underlining that “This is nothing new and has already been covered by a European Commission report in 2004. ALFI welcomes with interest this re-examination of current regulation”.

The first question to be asked is not the status of the depositary (One might think that Luxembourg is willing to eliminate the foreigner nonbanking competitors as circular IMF 91/75 states that “The admission to the activity of depositary of a UCITS subject to Part I of the Law of 30th March, 1988 is exclusively limited to banks incorporated under Luxembourg Law or Luxembourg branches of banks established in an EU Member State. This also applies to the depositary of a UCI subject to Part II of the Law of 30th March, 1988 save that such depositary may also be a Luxembourg branch of a bank established in a non Member State of the EU”). The French code requires that the depositary have his head office in France (Art. L. 214-16 of the UCIT Code).

The first question to be asked is definitely the risk of conflict of interests that are visible in Luxembourg and at the EU level in the decision-making process.

To conclude I will quote Fernand Grulms, who is head of Luxembourg For Finance.

He explains that Luxembourg wants “To be better known and recognized like a credible and reliable partner”. It is not by going on denying the poor governance in the jurisdiction that it will reach its objective.

09:20 Posted in Luxembourg | Permalink | Comments (0)

01/29/2009

The depositary issue is not a new thing

Almost 5 years ago the European Commission issued the following content in a Press Release (IP/04/430, dated 31/03/2004 ).

The Internet consultation flagged up significant gaps on, for example, minimum capital requirements, legal duties or the scope of liability for depositaries. A true Internal Market for depositary services will require convergence of these rules. In order to appoint depositaries based in other Member States, domestic fund managers and supervisors will want clarity on the resources of depositaries and on their obligations, whilst investors will need improved standards of information.

The Commission is therefore proposing close cooperation with EU regulators, covering four fields over the next two years.

1. Better prevention of conflicts of interests

Conflicts of interest arise when investors' interests are not at the heart of the depositary's or the fund manager's behaviour. The Commission survey revealed evidence of diverging approaches and it has therefore suggested action to boost convergence of national rules in this field. This includes the list of the functions that fund managers can outsource to depositaries and, conversely, the list of depositary activities which may be outsourced.

2. Clarifying the extent of the depositary's liability

Discrepancies in the level and scope of depositaries' liability constitute huge obstacles to ensuring a high level of investor protection throughout the EU and developing cross-border opportunities for depositaries. The Commission has identified as a key objective ensuring a common interpretation of the principal duty of depositaries which is to keep assets safe - and of the specific control duties assigned to them.

3. Convergence of prudential requirements

The prudential rules which must be applied to set up and operate a depositary differ considerably between Member States, since there are no common EU definitions of eligible institutions. The Commission proposes to foster convergence of these rules, and in particular of capital requirements, by identifying a specific group of relevant supervised institutions.

4. Enhancing transparency and investor information

In order to help create pressure to remove discrepancies in regulations, the Commission has identified the following areas for enhanced public information standards: the organisation of depositaries' tasks; measures taken against conflicts of interest; depositaries' liability; and the costs of their services.

The Madoff affair demonstrates that Luxembourg did not care of these Recs.

The Luxembourg financial center does not comply at all.

The Madoff affair demonstrates that the European Commission did not do its job.

06:00 Posted in General | Permalink | Comments (0)

01/25/2009

Pragmatic regulator

I have quoted circular IML 91/75 (as amended by Circular CSSF 05/177) to demonstrate that the depositary's liability is not as clear as what Luxembourg authorities are saying to reassure the investors.

This circular was modified by a recent circular that is definitely worrying for the investors.

CSSF circular 05/177 dated 6 April 2005 is relating to the abolition of any prior control by the CSSF of advertising material used by persons and companies supervised by the CSSF. (See original text in French)

It is a very short circular the wording of which is worth commenting.

Use of the verb Refrain

“the persons and companies subject to the supervision of the CSSF must continue to comply with the rules of conduct of the financial sector both in Luxembourg and abroad, in refraining from issuing misleading advertising material with regard to the services offered”

This means that It is up to the professional to decide not to circulate misleading Ads. The wording is not direct like “Misleading Ads are prohibited”. It is pragmatic.

Investor's liability

“by mentioning, where necessary, the particular risks inherent to these services and in bringing to the client's attention his own responsibility”

Furthermore a liability may be put on the investor as the professional is invited to mention the particular risks inherent to the services if necessary and bring to the client's attention his/her own responsibility.

When reading Luxalpha documentation it is written is the subscription form a clause, to be signed by investors or their agents, that states that assets would be “safekept” by a US broker – although it did not name Mr Madoff, and investors would bear most of the risk of that broker’s default. A suscription form is not an advertising material but why Luxalpha subscription form was circulated with such clause?

No sanction

“The control of the compliance with the rules of conduct of the financial sector regarding advertisement remains within the competence of the CSSF, which has the authority to require the withdrawal of any misleading advertisement with regard to the services offered as well as of any inappropriate communications of information on the Luxembourg legal framework”

The circular does not state a sanction, but only the withdrawal, which is not a sanction.

Above all, the circular states at the beginning that “advertising material used by persons in charge of the distribution of units of undertakings for collective investment and their representatives no longer needs to be submitted to the CSSF for their control, even if this material is not subject to control by the competent authorities in countries where it is used."

The European passport from Luxembourg is a threat as no control is done at all on the communication from Luxembourg investment funds.

In the context of the Madoff case, this means that the investor cannot trust anymore the communication from Luxembourg investment funds.

QED.

06:11 Posted in Luxembourg | Permalink | Comments (1)