09/16/2009

PwC: Who else?

The Chamber of Commerce and PwC published a brochure and a video to promote Luxembourg and PwC.

« Une vision pragmatique et réaliste d’un pays qui propose un cadre attractif et innovant pour établir et développer une entreprise en Europe » (a pragmatic and realistic vision of a country that offers an attractive and innovative framework to set up and develop a company in Europe), the Chamber of Commerce wrote.

There are testimonies of companies of which Paypal that is a PwC Client.

As Richard Murphy observed in June 2007, Pay Pal went to Luxembourg for all the wrong reasons:

Officially, tt was said that the transfer would enable management to market the service to online merchants across Europe and allow consumers to use PayPal in more places and ways across the web. Other eBay group companies, such as Skype and eBay, have an important presence in Luxembourg, so it makes sense for PayPal Europe to co-locate with them.”

Richard stated the three real reasons:

- Pay Pal would pay less tax;

- Pay Pal would not be as effectively regulated;

- Information exchange would be harder. Luxembourg tries hard not to play that game. And tax authorities are increasingly asking for data. If that information is located in the UK tax authorities can now get it. That will be harder from Luxembourg. It’s a tax haven that still promotes secrecy, after all.

We have seen with Madoff and Luxalpha that the regulation is perfectible in Luxembourg : professionals admit they influence the regulator in its duties : the small size of the jurisdiction creates the risk all the more than professionals decide what is to be done for the regulation:

“The Luxembourg Investment Fund Industry has regularly had a very close and direct say on the evolution of the Luxembourg prudential regulatory environment governing the collective Investment Industry (...) This influence has been exerted directly and indirectly by the lobbying initiatives taken on the level of the different professional associations, be it ALFI or ABBL , but also and more importantly, trough a direct association with the Luxembourg Supervisory Authorities by means of a number of standing committees" (Rafik Fischer, Vice Chairman, ALFI, in 2005)

This is confirmed by the CSSF: "The internal committees assist the CSSF in the analysis of the development of the different financial sector segments, give their advice on any question relating to their activities and participate in the drawing-up and the interpretation of regulations relating to their specific field."

In other words professionals require changes in the transposition of directives and other international texts whatever matter (AML, tax, audit...) and therefore influence the regulator in its duties.

What about Paypal as a Luxembourg-registered company in this so-called regulated center?

There are actually 6 companies registered:

1) PAYPAL (EUROPE) S.A R.L.

No Reg. de Commerce: B0127485

Forme juridique: Société à responsabilité limitée de droit luxembourgeois

Date de constitution: 18.4.2007

Adresse postale: 22, BOULEVARD ROYAL - LUXEMBOURG

2) PAYPAL (EUROPE) S.A R.L. ET CIE, S.C.A.

No Reg. de Commerce: B0118349

Forme juridique: Société en commandite par actions de droit luxembourgeois

Date de constitution: 28.7.2006

Adresse postale: 22, BOULEVARD ROYAL - LUXEMBOURG

3) PAYPAL (EUROPE) S.A.

No Reg. de Commerce: B0118349

Forme juridique: Société en commandite par actions de droit luxembourgeois

Date de constitution: 28.7.2006

Adresse postale: 22, BOULEVARD ROYAL - LUXEMBOURG

4) PAYPAL 2 S.A R.L.

No Reg. de Commerce: B0127758

Forme juridique: Société à responsabilité limitée de droit luxembourgeois

Date de constitution: 18.4.2007

Adresse postale: 22, BOULEVARD ROYAL - LUXEMBOURG

5) PAYPAL 3 S.A R.L.

No Reg. de Commerce: B0127484

Forme juridique: Société à responsabilité limitée de droit luxembourgeois

Date de constitution: 18.4.2007

Adresse postale: 22, BOULEVARD ROYAL - LUXEMBOURG

6) PAYPAL HOLDINGS S.A.

No Reg. de Commerce: B0118349

Forme juridique: Société en commandite par actions de droit luxembourgeois

Date de constitution: 28.7.2006

Adresse postale: 22, BOULEVARD ROYAL - LUXEMBOURG

Observations :

All have the same address: 22 boulevard Royal, Luxembourg.

There are actually 4 different numbers: B0118349, B0127758, B0127485, B0127484, B0118349 being repeated three times.

There are various status: 3 « Société en commandite par actions de droit luxembourgeois », 3 « Société à responsabilité limitée de droit luxembourgeois ».

The same individuals or legal persons appear for the registration process:

1. Mr Paul Mousel represented by Mr Max Kremer (1st company, 5th company)

2. 1) PayPal Global Holdings Inc., a company incorporated under the laws of Delaware, United States of America, having its registered office at 160 Greentree Drive, Suite 101 Dover, Delaware, United States of America; 2) PayPal Inc., a company incorporated under the laws of Delaware, United States of America, having its registered office at 160 Greentree Drive, Suite 101 Dover, Delaware, United States of America; both represented by Max Kremer (2nd company, 3rd company, 6th company)

3. PayPal PTE. LTD., a company incorporated under the laws of Singapore represented by Max Kremer (4th company)

Max Kremer and Paul Mousel are both from the law firm Arendt & Medernach:

Paul Mousel is a founding partner of the firm and presently serves as head of the firm’s industry group “Multi-national Companies (MNC) and public sector”. He is a partner in both the Banking and Financial Services and the Insurance and Reinsurance Practices where he specialises in securities law, regulatory matters involving banks, investment firms, insurance and reinsurance companies as well as all aspects of organisation, reorganisation, mergers & acquisitions and liquidation of financial institutions. He is the Chairman of the Management Board of Arendt & Medernach. He has been a member of both the Luxembourg and Brussels Bar since 1978. He is a member of the Banking Committee of the Commission de Surveillance du Secteur Financier (CSSF), the regulatory authority of the financial sector in Luxembourg, and also acts as a non-executive board member in numerous companies.

Max Kremer is a senior associate in the Banking and Financial Services Practice where he specialises in corporate and regulatory matters involving banks, investment firms, insurance and reinsurance companies. He advises on all aspects of organisations, reorganisations, mergers & acquisitions, migrations and liquidations of financial institutions. He has been a member of the Luxembourg Bar since 2004. He is a reader of general commercial law at the Luxembourg Chamber of Commerce.

Legal persons come from jurisdictions that are considered as tax havens:

- Delaware (2nd company, 3rd company, 6th company) is considered as a tax haven by professionals and politicians in Luxembourg (e.g. : “The tax-friendly US states of Delaware, Nevada and Wyoming should figure on an international blacklist of offshore tax havens” (Jean-Claude Juncker)

- Singapore ((4th company) remains in the OECD grey list dated 15 September 2009 far away from the 12 required agreements.

Luxembourg must be better, much better, than both jurisdictions as a tax haven…

It is in the European Union and has therefore the advantages of both an onshore and an offshore jurisdiction.

17:23 Posted in Luxembourg | Permalink | Comments (0)

FINMA presents report on the financial market crisis

The “Financial market crisis and financial market supervision” that was published the day before yesterday by FINMA provides a comprehensive analysis of the financial market crisis and the ensuing decisions and actions taken by the Swiss Federal Banking Commission (SFBC). None of those involved recognised in time the origins of the crisis or the full extent of the dangers it posed. Furthermore, the analysis reveals certain weaknesses and a partial lack of effectiveness in banking supervision. The report concludes, however, that the SFBC responded rapidly and decisively, and that fundamental decisions for stabilising the financial centre were made in a targeted and timely manner. The SFBC quickly learned its lessons from the crisis and implemented remedial actions.

Read summary of the report (English)

05:35 Posted in Switzerland | Permalink | Comments (0)

09/15/2009

Luxembourg: a prime location for locating non substantial activities

The H29 is ending. As the OECD observes in OECD Economic Surveys: Luxembourg 2008, “The 1929 holding (H29) was a vehicle for holding capital and enjoyed a favourable tax regime, in return for which its range of activities was confined to taking participations in other companies, managing bond loans, and managing patents and licences under certain conditions. The holding was not allowed to engage in any commercial activities, failing which it would forfeit its tax regime. In 2006 the European Commission found the new H29 tax regime to be non-compliant with European legislation on State aid, leading to the government

decision to phase out the scheme by 2010. H29s were excluded from double taxation treaties and were not allowed to benefit from the tax regime common to parent companies and their subsidiaries resident in the European Union. This characteristic therefore restricted the use of H29s as vehicles in international acquisition structures. These structures were in fact mainly used by private individuals as wealth management products.

As Arnaud Bourgain, Patrice Pieretti and Jens Høj observes in their report titled “CAN THE FINANCIAL SECTOR CONTINUE TO BE THE MAIN GROWTH ENGINE IN LUXEMBOURG?”, in 2007, a new form of finance company was introduced – the private asset management company or Société de gestion de Patrimoine Familial (SPF) – to replace the so-called 1929 holding legislation (H29).The tax regime applying to SPFs is essentially the same as in the case of H29 companies (no tax on dividends paid, no municipal business tax or net wealth tax, liability to the capital duty tax (droit d’apport) of 0.5% (which will be abolished in 2009) and to the yearly subscription tax of 0.25%, no access to double taxation treaties, etc.). However, SPFs are available only to private individuals (or intermediaries acting in the interests of an individual or a group of individuals) and their sole purpose is the administration and management of financial assets, excluding any form of commercial activity. The restriction to private individuals should make the SPFs compliant with European State aid rules. Other legislative changes were already implemented in 1990 to allow setting up so-called SOPARFIs (Sociétés de Participations Financières) to remedy the limitations of the 1929 holding company as an international financial engineering vehicle. They are ordinary commercial companies not liable to the restrictions applying to company aims and not benefitting from tax exemption on profits. A SOPARFI can therefore pursue all the activities open to SPFs, but can also have an activity related to the management of its participations (advice on management, financing, real estate, etc.) or any other commercial or industrial

activity. One advantage for foreign investors of this type of company is to repatriate investments in foreign companies /subsidiaries to the company in Luxembourg and become subject to Luxembourg’s tax rules, with the aim of distributing the investment income to shareholders. As a consequence of being fully liable to tax, the SOPARFIs benefit from double-taxation treaties and the parent-subsidiary directive. A common tax regime for the parent company and the subsidiary allows distributed dividends to be tax-exempt (and in some cases also from withholding tax) in the country where the parent company is located.

Soparfi are not in question but they are part of Financial engineering through Luxembourg that do not abide by foreign tax administrations rules, with the example of litigations in France.

A recent jurisprudence of the Conseil d’Etat in France considers that there was abuse of law for a structure that was created in Luxembourg. Other research demonstrates that there are actually several litigations involving the same Luxembourg-based company.

Caisse Interfédérale de Crédit Mutuel (Conseil d’Etat, 27 Juillet 2009) : « (…) Considérant que le ministre soutient, sans être sérieusement contredit, que les deux holdings de droit luxembourgeois Europarticipations et Europartiaire sont restées, au cours de leur période d'existence, sous l'entière dépendance de la Banque Internationale du Luxembourg, à l'origine de leur création en ce qui concerne tant leur gestion que leurs investissements, que la totalité de leurs actifs était constituée de valeurs mobilières, qu'elles n'avaient aucune compétence technique en matière de placements financiers, que leurs actionnaires ne prenaient aucune part aux assemblées statutaires et qu'ainsi ces sociétés étaient dépourvues de toute substance (…) »

Société Conforama Holding (Conseil d’Etat, 27 Juillet 2009) : « (…) Considérant qu'en estimant insuffisante, par une appréciation souveraine, la valeur probante des éléments apportés par la société pour contredire l'argumentation de l'administration fiscale selon laquelle le montage auquel avait participé la société requérante avait pour but exclusif d'éluder l'impôt, la cour, qui a relevé que le ministre soutenait, sans être sérieusement contredit, que la société Europarticipations était restée au cours de sa période d'existence sous l'entière dépendance de la Banque Internationale du Luxembourg, à l'origine de sa création, en ce qui concerne tant sa gestion que ses investissements, qu'elle ne constituait qu'une structure dépourvue de substance dès lors que son conseil d'administration n'était composé que de membres dirigeants de cette banque (…) »

Société par actions simplifiées BHV (CAA-Paris, 17 avril 2008) : « (…) Considérant que l’administration fait valoir que la société Europarticipations est restée, au cours de la période en litige, sous l’entière dépendance de la Banque Internationale du Luxembourg, établissement bancaire à l’origine de sa création, en ce qui concerne tant sa gestion que ses investissements, que la totalité de ses actifs était composée de valeurs mobilières, qu’elle n’avait aucune compétence technique en matière de placements financiers, que ses actionnaires ne prenaient aucune part aux assemblées statutaires et qu’ainsi cette société était dépourvue de substance, son conseil d’administration n’étant composé que de membres dirigeants de l’établissement bancaire (…) »

Société Anonyme des Galeries Lafayettes (CAA-Paris, 23 avril 2007 ) : « (…) Considérant que l'administration fait valoir que la société Europarticipations est restée, au cours de la période en litige, sous l'entière dépendance de la Banque Internationale du Luxembourg, établissement bancaire à l'origine de sa création, en ce qui concerne tant sa gestion que ses investissements, que la totalité de ses actifs était composée de valeurs mobilières, qu'elle n'avait aucune compétence technique en matière de placements financiers, que ses actionnaires ne prenaient aucune part aux assemblées statutaires, et qu'ainsi, cette société était dépourvue de substance, son conseil d'administration n'étant composé que de membres dirigeants de l'établissement bancaire (…) »

Société Conforama Holding (CAA-Paris - 22 mai 2006) : « (…) Considérant que le ministre de l'économie, des finances et de l'industrie soutient, sans être sérieusement contredit, que la société de droit luxembourgeois Europarticipations est restée, au cours de sa période d'existence, sous l'entière dépendance de l'établissement bancaire à l'origine de sa création, tant en ce qui concerne sa gestion que ses investissements, et qu'elle ne constituait qu'une structure intermédiaire dépourvue de substance, son conseil d'administration n'étant composé que de membres dirigeants de cet établissement ; qu'en outre, les actionnaires français, associés de cette société, ne présentaient aucune communauté d'intérêt, en raison de leurs activités disparates, n'exerçant aucune influence sur la gestion des actifs par celle-ci (…) »

Caisse Interfédérale de Crédit Mutuel (CAA-Nantes, 2 main 2006) : « (…) Considérant que l'administration fait valoir que les sociétés Europartiaire et Europarticipation sont restées, au cours de la période en litige, sous l'entière dépendance de la Banque Internationale du Luxembourg, établissement bancaire à l'origine de leur création, en ce qui concerne tant leur gestion que leurs investissements, que la totalité de leurs actifs était composée de valeurs mobilières, qu'elles n'avaient aucune compétence technique en matière de placements financiers, que leurs actionnaires ne prenaient aucune part aux assemblées statutaires, et qu'ainsi, ces sociétés étaient dépourvues de substance (…) »

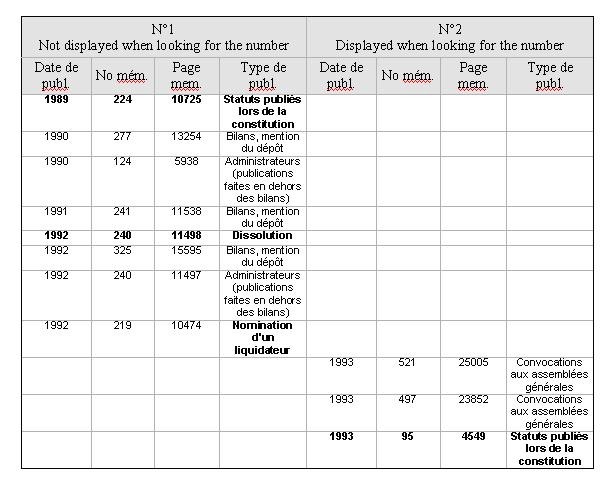

What can be seen in the Corporate Registration about the Luxembourg-based company is interesting.

The company appears twice in the Mémorial C

1) EUROPARTICIPATIONS SA

No Reg. de Commerce:

Forme juridique: Société holding sous forme de société anonyme

Date de constitution: 8.3.1989

Adresse postale: 2, BD. ROYAL

LUXEMBOURG

2) EUROPARTICIPATIONS SA

No Reg. de Commerce: B0042226

Forme juridique: Société anonyme de droit luxembourgeois

Date de constitution: 27.11.1992

Adresse postale: 65, RUE DES ROMAINS

STRASSEN

Its number (No Reg. de Commerce) is not specified for the first company.

There are parallel actions in « both companies »

Exemple :

For the first one:

| 7.9.2000 | Bilans, mention du dépôt |

For the second one :

| 19.12.2001 | Bilans, mention du dépôt |

| 3.9.1998 | Administrateurs et changement adresse |

In fact the first one, that does not have the number displayed, has the same number as the other one. But when one makes a research with the number only the actions of the second company are displayed.

The split sounds strange.

When one builds a synoptic table, it appears that the company was dissolved then liquidated then created again.

Such resurrection is the miracle of the business law in Luxembourg all the more than the litigious tax behaviour in France took place prior to the dissolution.

More seriously, there are many red flags in the Corporate Registration and whenever there are anomalies in a company’s publications there is a dubious situation. See for example Eurolux that I analysed one year ago : this Luxembourg-based company would have been used to bypass the OECD Anti-Bribery Convention as the starting hub. The company went bankrupt.

Anomalies are tolerated in Luxembourg.

The Luxembourg tax haven is there. It is bared.

07:22 Posted in Luxembourg | Permalink | Comments (0)