06/11/2009

A telling censorship of Luxembourg professionals on issues relating to the depositary's liability

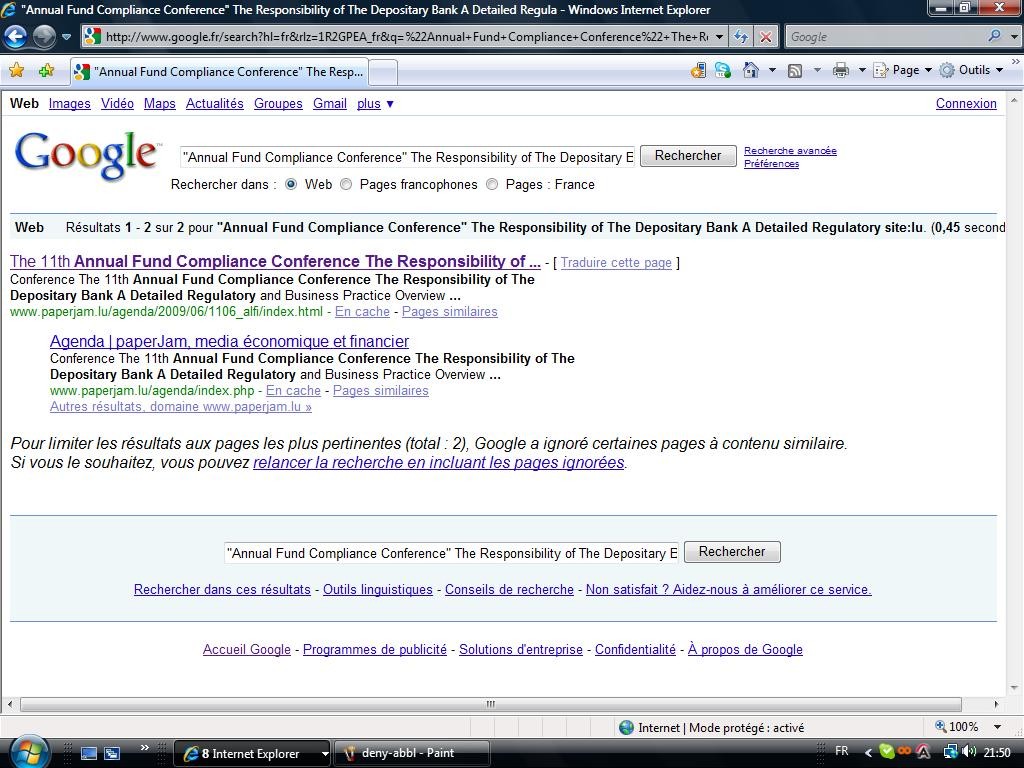

Today and tomorrow is taking place in Luxembourg the 11th Annual Fund Compliance Conference on the topic : The Responsibility of The Depositary Bank A Detailed Regulatory and Business Practice Overview

In the Ad, it is said that the European Commission will highlight the Commission Approach with regards to “Depositary Responsibilities”.

The conference will give a detailed regulatory and business practice overview of “The Responsibility of The Depositary Bank” and will provide a lively debate on how to build on shared and mutually reinforcing responsibilities The Role, Responsibility and Liability of The Depositary Function and its Delegation.

Indeed, there are differences in approaching depositary duties across Europe and consequences from the financial crisis have pledged for a strengthening of the functioning of the financial markets.

A panel session will give the views from Fund Board Members on their role and responsibility vis à vis a substantive oversight of the fund that includes the supervision of the depositary duties.

Finally the conference will assess whether UCITS IV generation is addressing adequately depositary duties and how the various scenarios of the Management Company Passport will impact the functioning of the depositary duties.

It is very amazing that the conference on a sensitive topic for Luxembourg is like boycotted by the Luxembourg financial community. It is a consent that the legal and regulatory framework on the depositary is in question in Luxembourg.

Such behaviour is worrying for investors.

A Google search shows that there is only one article about the conference for site:lu:

The 11th Annual Fund Compliance Conference on the topic : The Responsibility of The Depositary Bank A Detailed Regulatory and Business Practice Overview is not promoted by the ALFI, the official representative body for the Luxembourg investment fund industry. Strange.

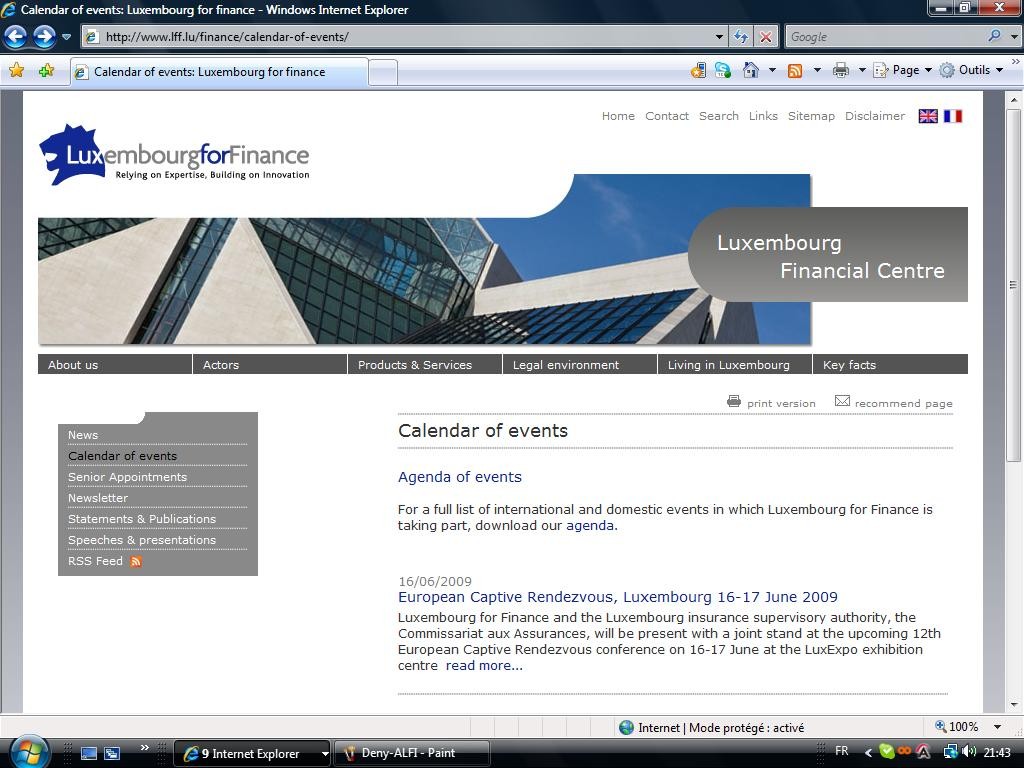

The 11th Annual Fund Compliance Conference on the topic : The Responsibility of The Depositary Bank A Detailed Regulatory and Business Practice Overview is not promoted by Luxembourg For Finance, the agency for the development of the financial sector. Strange.

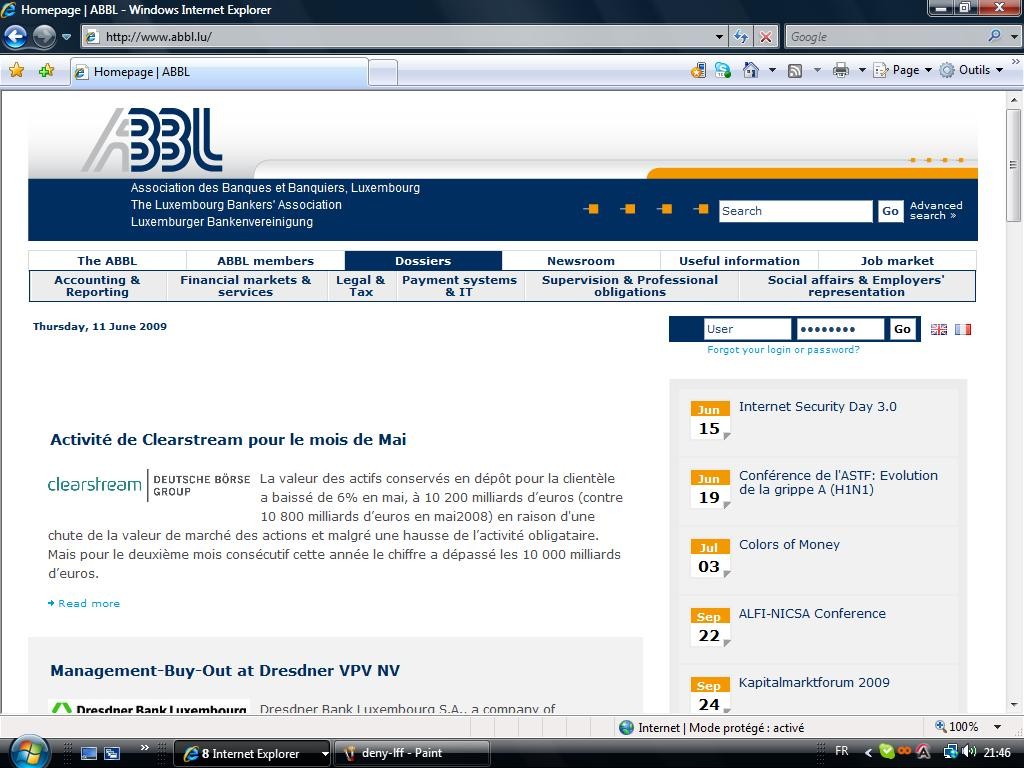

The 11th Annual Fund Compliance Conference on the topic : The Responsibility of The Depositary Bank A Detailed Regulatory and Business Practice Overview is not promoted by the ABBL, the Luxembourg Bankers' Association. Strange.

21:55 Posted in Luxembourg | Permalink | Comments (0)

06/10/2009

The head of the Luxembourg bankers' association recently admitted that Luxembourg was a tax haven

In a recent interview, Jean Meyer stated that "le Luxembourg doit sortir de cette image de paradis fiscal, de refuge pour patrimoines non déclarés, qui ne correspond plus à son identité" (free transmation : Luxembourg must leave this image of tax haven, of refuge for not declared assets, which does not correspond anymore to its identity)

This sentence wants a couple of comments.

It is the first time that a Luxembourg powerhouse admits that Luxembourg's identity was a tax haven and a place for not declared assets but it is no longer the case: it not correspond anymore to its identity

I can consider from a semantic point of view that Mr Meyer is officially repudiating what stated Jean Jacques Rommes in February 2009 or Lucien Thiel in February 2008.

He takes into account the commitments to counter tax evasion.

19:10 Posted in Luxembourg | Permalink | Comments (0)

Good governance in tax matters in the European Union

The Council of the European Union yesterday adopted conclusions on good governance in the tax area.

What was said is the following (I have added bold style):

- The Council takes note of the Commission Communication on promoting good governance in tax matters (9281/09) presented to the Council on 5 May 2009 and, subsequent to its May 2008 Conclusions, recalls the importance of implementing the good governance tax principles of transparency, exchange of information and fair tax competition as a means of ensuring a level playing field and of combating cross border tax fraud and evasion.

- The Council welcomes the suggestion in this Communication to accelerate the ongoing work on legislative proposals concerning the savings taxation directive (15733/08), the administrative cooperation directive (6035/09) and the recovery directive (6147/09).

- The Council is committed to further discuss and promote the principle of good governance in the tax area at international level and towards third countries without prejudice to Community and Member States’ competences. It recalls the March 2009 European Council joint position that refers in this respect to the fight against tax evasion and the application of appropriate and gradual countermeasures towards uncooperative third country jurisdictions.

- Recalling the Council Conclusions of 10 February 2009 the Council urges the Commission to swiftly present the negotiating result on the anti-fraud agreement with Liechtenstein. The Council notes the intention of the Commission to present negotiating directives for anti-fraud agreements with Monaco, Andorra, San Marino and Switzerland.

- The Council welcomes the emerging broad international consensus on the need to enhance administrative cooperation and mutual assistance in the tax area and to apply the OECD standard as regards exchange of information on request (Article 26 paragraphs 4 and 5 OECD Model Convention), i.e. that provision of information can no longer be refused on the sole ground that the information is held by certain financial institutions, or on the sole ground that the requested state has no domestic interest in such information.

- More specifically, as regards the ongoing review of the savings taxation directive, the Council notes the Presidency progress report. It welcomes the progress made and agrees that circumvention of savings taxation should be prevented and that the functioning of savings taxation should be improved in the framework of an overall agreement in particular by:

§ an extension of the scope of the Directive to at least other substantially equivalent income than just interest from savings,

§ the introduction of a look through approach for payments to certain non-EU entities and arrangements and a more systematic application of paying agent upon receipt responsibilities, and

§ a broader use of personal identification numbers and the use of the information on actual tax residence, when available, in identification procedures.

It calls for a rapid continuation of work in order to find constructive solutions to outstanding issues, among others possible options for covering certain insurance products, detailed provisions to ensure the coverage of certain untaxed entities and arrangements within the EU and in the dependent and associated territories as well as questions on further decision making. The work should continue with a view to reaching a balanced political agreement in the autumn of 2009.

The Council also calls on the Commission to open consultations with Switzerland, Liechtenstein, Andorra, Monaco and San Marino on revising their respective agreements on savings taxation with the aim to ensure application of equivalent measures in line with international standards and the improvements agreed at EU level.

The Council encourages Member States with dependent or associated territories to consult with them to apply the same measures in the area of savings taxation as will apply at EU level.

The Council recalls that the issue of the transitional period remains to be addressed in accordance with Article 10 paragraph 2 of Directive 2003/48/EC subject to the conditions set out therein.

- The Council also welcomes the proposals for the directives on administrative cooperation and recovery, expanding their scope as regards taxes and duties covered, simplifying the exchange of information by means of standardised forms, formats and channels of communication and facilitating recovery by using new or improved instruments. The Council stands ready to examine both proposals further and to continue its efforts in the autumn of 2009 to find solutions to outstanding issues that are fully consistent with the OECD standard (Article 26 OECD Model Convention).

- The Council invites the future Presidency to report back on progress in the area of good governance in tax matters in the autumn of 2009.

What is said?

Ø The Savings Directive is being reviewed and especially the principle of the transitional period is recalled: Belgium, Luxembourg and Austria will have to give up their legislation.

Ø A possible global agreement with Third Countries on the tax information exchange is sought.

06:54 Posted in General | Permalink | Comments (0)