05/17/2009

The community of we the others

In a recent interview in German, Luc Frieden, the Luxembourg Luc Frieden, Minister of Treasury and Budget, stated that “Wir sind ein internationaler Finanzplatz, der internationale Regeln liebt. Und es gibt internationale Regeln zum Steuerparadies. Das ist nach OECD-Regeln ein Ort, an dem man keine oder fast keine Steuern zahlt. Das trifft auf Luxemburg nicht zu. Deshalb möchten wir, dass die Beschreibung unseres Staates der Realität entspricht, und das ist nicht immer der Fall”, which means (free translation) “We are an international financial center, which abides by international rules. And there are international rules to define tax havens. That is according to OECD rules, a place where one pays no or nearly no taxes. That does not apply to Luxembourg. Therefore we would like that the description of our state corresponds to the reality, and that is not always the case”

A couple of comments about the reality of the state:

When Luc Frieden states that a tax haven is according to OECD rules, "a place where one pays no or nearly no taxes”, it is not accurate.

According to the OECD, four key factors are used to determine whether a jurisdiction is a tax haven. The first is that the jurisdiction imposes no or only nominal taxes. This is what Frieden has in mind.

But the OECD adds that the no or nominal tax criterion is not sufficient, by itself, to result in characterisation as a tax haven as the OECD recognises that every jurisdiction has a right to determine whether to impose direct taxes and, if so, to determine the appropriate tax rate. An analysis of the other key factors is needed for a jurisdiction to be considered a tax haven. The three other factors to be considered are:

- Whether there is a lack of transparency

- Whether there are laws or administrative practices that prevent the effective exchange of information for tax purposes with other governments on taxpayers benefiting from the no or nominal taxation.

- Whether there is an absence of a requirement that the activity be substantial

The description of his state that corresponds to the reality is that:

There is no culture of transparency: otherwise PwC and E&Y in Luxembourg would have participated to « Global Economic Crime Survey » for PwC and « Corruption or compliance – weighing the costs » for E&Y. These surveys are even not communicated. Otherwise there would be a balance sheet database like in any modern democracy. Otherwise there would be a database of judiciary judgements like in any modern democracy. And so on.

There are laws or administrative practices that prevent the effective exchange of information for tax purposes. In a speech before the Luxembourg Parliament on 13 March 2009, Luc Frieden announced that Luxembourg will conclude Double Taxation Agreements that conform to the OECD Model Tax Convention., which means that this was not the case before. Conventions are being signed.

But it remains that the request of information must be made on concrete, clear and precise evidence of tax evasion which excludes any “fishing expedition”. This is a problem in Luxembourg as leaders support tax evasion:

- Cf. what stated Lucien Thiel, former director of the Luxembourg Bankers’ Association: “It is not our duty to control if the taxpayer was honest” (L’Essentiel, 27 February 2008)

- Cf. what stated Jean-Jacques Rommes, current director of the Luxembourg Bankers’ Association to comment a tax evasion case: “It is not the banker who started” (RTBF, 19 February 2009)

Banking administrative practices actually prevent the effective exchange of information for tax purposes (Additionally in a connected field, which is AML, 60% of banks never report declarations of suspicion according to the Luxembourg FIU and ratios of comparison with other jurisdiction demonstrate a poor level of declarations of suspicion in Luxembourg : Cf. for example the comparison with Monaco).

There is an absence of a requirement that every activity be substantial. The Luxembourg corporate registration is full of Luxembourg-based companies that are linked to exotic jurisdictions and that exist only in the Luxembourg Corporate registration. In the tax evasion case Jean-Jacques Rommes was asked to comment on the banker who suggested a scam through Panama without even being asked to do so by the client.

At the time when the USA seem to be willing to ensure that U.S. states like Delaware and Nevada do not replace offshore countries like Switzerland, Luxembourg and the Cayman Islands as tax havens for wealthy individuals and businesses, Luxembourg goes on ignoring the paradigm shift in the world.

This it is not very good omen for the Luxembourg Institute For Global Financial Integrity, that is said to be intended to solve the challenges faced by the global financial sector pertaining to crime, such as fraud, tax evasion, and money laundering, and to the funding of criminal activity and terrorism.

18:36 Posted in Luxembourg | Permalink | Comments (0)

Bad news for Luxembourg but good news for responsible financial actors

Richard Murphy has reported that Las Vegas Review wrote that President Barack Obama’s plan to limit tax breaks for multinational companies will include an amendment that affects alleged tax havens at home, including Nevada and Delaware, a knowledgeable source in Washington, D.C., said. The yet-to-be-announced amendment will make sure that U.S. states do not replace offshore countries like Switzerland, Luxembourg and the Cayman Islands as tax havens for wealthy individuals and businesses, the source explained.

As the existence of Delaware and Nevada was the only argument that Luxembourg politicians and officials found to avoid the handing-over in question, it is a new example of the bad approach of this jurisdiction that need homines novi (new leaders).

09:17 Posted in General | Permalink | Comments (0)

05/15/2009

Launch of the Luxembourg Institute For Global Financial Integrity: good initiative but questions remain…

The Luxembourg Institute for Global Financial Integrity announced its constitution yesterday. Founded by private citizens from Europe and The United States, under the auspices of Jacques Santer, former Prime Minister of Luxembourg and President of the European Commission, the institute is a nonprofit organization, that addresses the integrity of the global financial sector and the social responsibility practiced by all of its stakeholders.

According to Mr. Santer, "We recognized that the global financial sector is in need of stronger ethical practices and standards based on the principles of integrity: transparency, fairness, responsibility and accountability".

Jean-Claude Juncker, Prime Minister of Luxembourg, has given his personal endorsement and support to the institute in recognition of the need for a private, independent and impartial body that will group corporate, academic and non-governmental organizations, in Luxembourg and abroad who are engaged in the global financial sector, together to solve the challenges faced by the global financial sector pertaining to crime, such as fraud, tax evasion, and money laundering, and to the funding of criminal activity and terrorism.

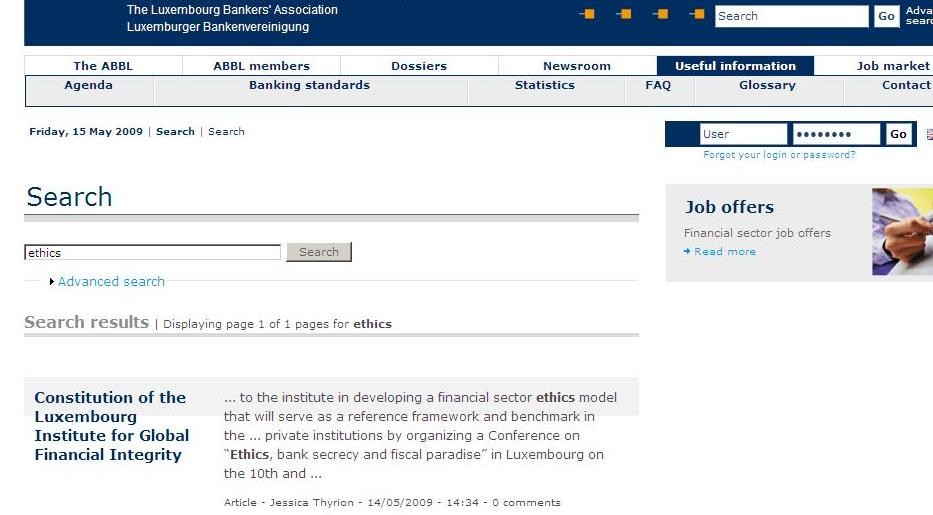

The institute announced that in one of its first projects, Howard Gardner, Hobbs Professor of Cognition and Education of the Harvard Graduate School of Education, will advise and contribute to the institute in developing a financial sector ethics model that will serve as a reference framework and benchmark in the development of the ethical code of conduct of the global financial sector and the work that will later be carried out by the Institute.

As a newly created nonprofit organization, The Luxembourg Institute for Global Financial Integrity, is now enrolling members who will be active in all aspects of the institute. Banks, institutions and service providers in the global financial markets are being invited to join the institute. Research Fellows and Visiting Research Fellows are being sought out and brought on board. Collaboration is being established with universities, think-tanks and nongovernmental organizations (NGOs) engaged in social responsibility and transparency within the global financial sector.

The institute will initiate its first open dialogue within the global financial sector and with public and private institutions by organizing a Conference on "Ethics, bank secrecy and fiscal paradise" in Luxembourg on the 10th and 11th of December, 2009.

A couple of comments:

I definitely welcome the launch of such institute in Luxembourg, which meets two of my observations relating to the Luxembourg jurisdiction:

- As I demonstrated, business ethics was not taken into account in Corporate Social Responsibility as implemented in Luxembourg. The scope of the institute is consistent with the scope of the ORSE in the identification of issues and responsibilities specific to banks, insurance companies and asset managers. I understand that it is a special body for CSR in the financial sector. Better late than never.

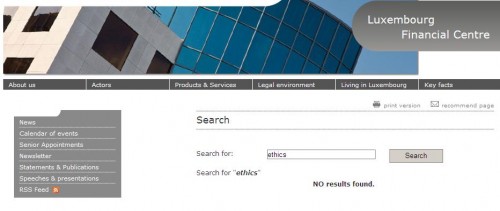

Ethics was not a concern for bankers in Luxembourg before the launch of the institute as there is only one result for the keyword: the one of the institute:

- As I explained, despite an international labor, Luxembourg was locked up in internal visions disconnected from realities from the world and lack thus of true pragmatism, pragmatism being a practical approach to problems and affairs ; otherwise they would have realised the paradigm shift mid 2000. The institute is open to the world.

Additionally, the sort and the wording of the scope is interesting: "to solve the challenges faced by the global financial sector pertaining to crime, such as fraud, tax evasion, and money laundering, and to the funding of criminal activity and terrorism" : AML-CFT come last as the current issue is fraud and tax evasion quoted firstly.

Nevertheless a couple of issues remain, of which:

Will the institute be a tool to change the business culture or is it an opportunist ethical frontage for the center? A clue to assess the credibility is the project team: is the project team relevant to promote stronger ethical practices and standards based on the principles of integrity: transparency, fairness, responsibility and accountability. Should there be team members involved in corruption issues or promotion of fraud or tax evasion or other dubious business behaviour (verifiable public lie to mislead the investors...), the institute would not be credible. Another clue will be the capacity to welcome "critics" especially when they lay emphasis on public and official dysfunctions that are the visible part of the iceberg. The word critic comes from the Greek κριτικός (kritikós), "able to discern", which in turn derives from the word κριτής (krités), meaning a person who offers reasoned judgment or analysis, value judgment, interpretation, or observation. In practice critics are blacklisted in the Luxembourg business.

How the institute will handle specific issues in Luxembourg due to the small size: conflicts of interest that can turn into corruption defined as an impairment of integrity, virtue, or moral principle? Luxembourg is a small jurisdiction where everybody knows everyone, where officials and ministers are reachable, etc.

How the institute will handle issues relating to businesses that do not belong to the financial sector but may cause a collateral damage for the reputation of the financial sector:

- Creation of scams connected to exotic jurisdictions on the OECD "grey list",

- Anybody can be a statutory auditor including exotic firms from the BVI, the Seychelles and so on, that are not controlled,

- etc.

In a nutshell, I am available to join the institute to which I want to give the credit at the beginning.

But as I am not a yes-man, as I have an independent mindset and as I have a true pragmatism based on facts, I don't think I will be welcome among the Research Fellows and Visiting Research Fellows that are sought.

17:30 Posted in Luxembourg | Permalink | Comments (0)